[ad_1]

Generative AI (GenAI) has the potential to rework the insurance coverage business by offering underwriters with helpful insights within the areas of 1) danger controls, 2) constructing & location particulars and three) insured operations. This expertise might help underwriters establish extra worth within the submission course of and make higher high quality, extra worthwhile underwriting choices. Elevated score accuracy from CAT modeling means higher, extra correct pricing and lowered premium leakage. On this submit, we’ll discover the chance areas, GenAI functionality, and potential influence of utilizing GenAI within the insurance coverage business.

1) Danger management insights zone in on materials knowledge

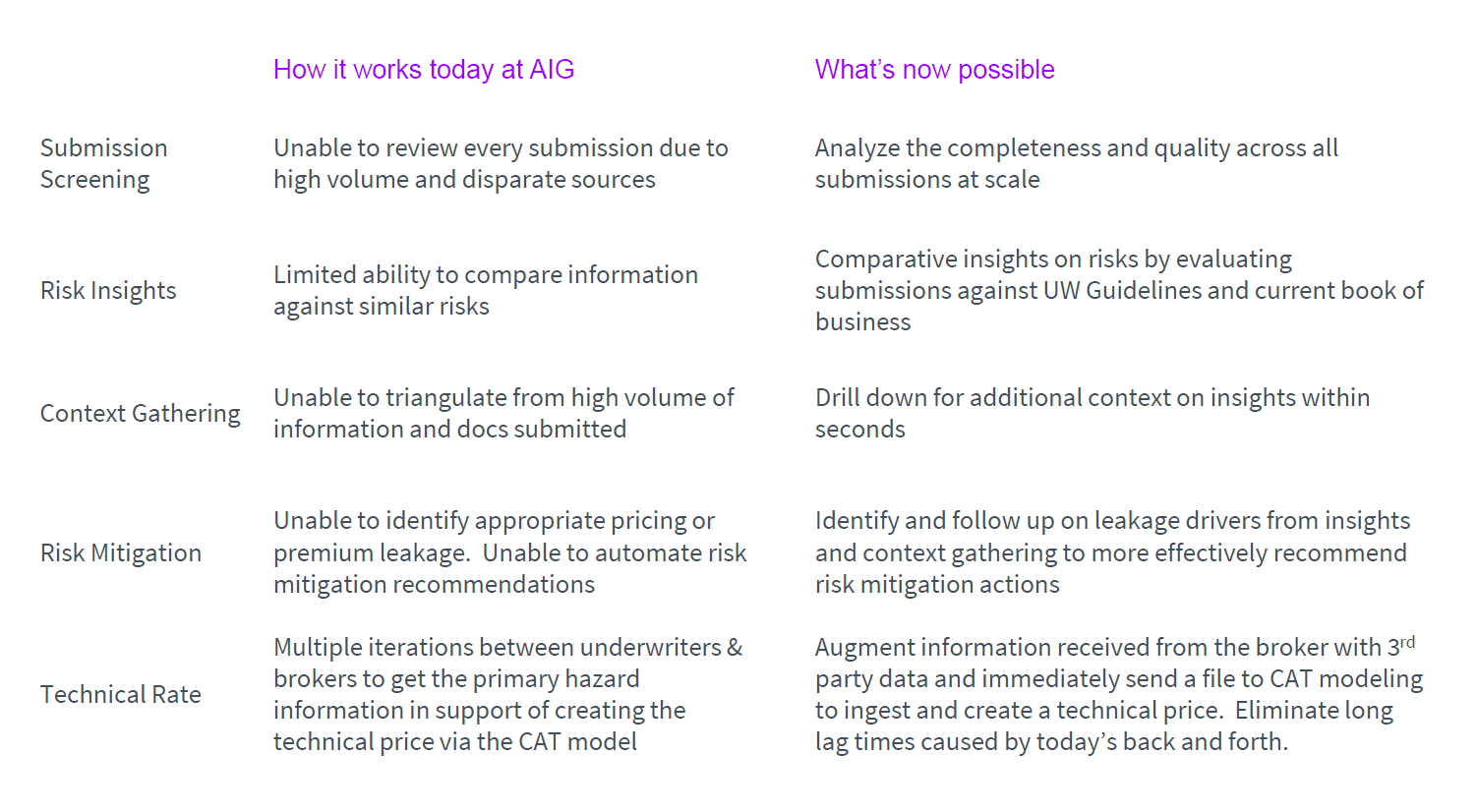

Generative AI permits risk management evaluation insights to be highlighted to indicate loss prevention measures in place in addition to the effectiveness of these controls for decreasing loss potential. These are important to knowledgeable underwriting choices and might handle areas which can be persistently missed or ache factors for underwriters in knowledge gathering. At present with regards to submission screening, underwriters are unable to evaluation each submission as a consequence of excessive quantity and disparate sources. Generative AI permits them to analyze the completeness and high quality throughout all submissions at scale. Because of this they transfer from a restricted skill to match data towards related dangers to a situation the place they’ve comparative insights on dangers by evaluating submissions towards UW Pointers and present e book of enterprise.

What generative AI can do:

- Generate a complete narrative of the general danger and its alignment to carriers’ urge for food and e book

- Flagging, sourcing and figuring out lacking materials knowledge required

- Managing the lineage for the info that has been up to date

- Enriching from auxiliary sources TPAs/exterior knowledge (e.g., publicly listed merchandise/providers for insured’s operations)

- Validating submission knowledge towards these further sources (e.g., geospatial knowledge for validation of vegetation administration/proximity to constructing & roof development supplies)

Synthesizing a submission bundle with third occasion knowledge on this method permits it to be introduced in a significant, easy-to-consume method that in the end aids decision-making. These can all enable sooner, improved pricing and danger mitigation suggestions. Augmenting the knowledge acquired from the dealer with third occasion knowledge additionally eliminates the lengthy lag occasions brought on by in the present day’s forwards and backwards between underwriters and brokers. This may be taking place instantly to each submission concurrently, prioritizing inside seconds throughout your entire portfolio. What an underwriter may do over the course of every week may very well be carried out instantaneously and persistently whereas making knowledgeable, structured suggestions. The underwriter will instantly know management gaps primarily based on submission particulars and the place important deficiencies / gaps might exist that might influence loss potential and technical pricing. In fact, these should then be thought of in live performance with every insured’s particular person risk-taking urge for food. These enhancements in the end create the flexibility to put in writing extra dangers with out extreme premiums; to say sure while you may in any other case have mentioned no.

2) Constructing & Location particulars insights support in danger publicity accuracy

Let’s take the instance of a restaurant chain with a number of properties that our insurance coverage provider is underwriting for instance constructing element insights. This restaurant chain is in a CAT-prone area comparable to Tampa, Florida. How may these insights be used to complement the submission to make sure the underwriter had the total image to precisely predict the chance publicity related to this location? The high-risk hazards for Tampa, based on the FEMA’s Nationwide Danger Index, are hurricanes, lightning, and tornadoes. On this occasion, the insurance coverage provider had utilized a medium danger stage to the restaurant as a consequence of:

- a previous security inspection failure

- lack of hurricane safety models

- a possible hyperlink between a previous upkeep failure and a loss occasion

which all elevated the chance.

Alternatively, in preparation for these hazards, the restaurant had carried out a number of mitigation measures:

- necessary hurricane coaching for each worker

- steel storm shutters on each window

- secured outside objects comparable to furnishings, signage, and different free objects that might grow to be projectiles in excessive winds

These had been all added to the submission indicating that they’d the mandatory response measures in place to lower the chance.

Whereas constructing element insights expose what is actually being insured, location element insights present the context during which the constructing operates. Risk management evaluation from constructing value determinations and security inspection studies uncover insights exhibiting which places are the highest loss driving places, whether or not previous losses had been a results of lined peril or management deficiency, and adequacy of the management techniques in place. Within the case of the restaurant chain for instance, it didn’t have its personal hurricane safety models however based on the detailed geo-location knowledge, the constructing is situated roughly 3 miles away from the closest fireplace station. What this actually means is that when it comes to context gathering, underwriters transfer from being unable to triangulate from excessive quantity of knowledge and paperwork submitted to having the ability to drill down for added context on insights inside seconds. This in flip permits underwriters to establish and comply with up on leakage drivers from insights and context gathering to advocate danger mitigation actions extra successfully.

3) Operations insights assist present suggestions for added danger controls

Insured operations particulars synthesize data from the dealer submission, monetary statements and knowledge on which features usually are not included in Acord kinds / functions by the dealer. The hazard grades of every location related to the insured’s operations and the predominant and secondary SIC codes would even be offered. From this, rapid visibility into loss historical past and prime loss driving places in contrast with complete publicity might be enabled.

If we take the instance of our restaurant chain once more, it may very well be attributed a ‘excessive’ danger worth relatively than the aforementioned ‘medium’ because of the truth that the location has potential dangers from e.g. catering supply operations. By analyzing the operation publicity, that is how we establish that prime danger in catering :

The utmost occupancy is excessive at 1000 individuals, and it’s situated in a buying advanced. The variety of claims during the last 10 years and the typical declare quantity may additionally point out the next danger for accidents, property injury, and legal responsibility points. Though some danger controls might have been carried out comparable to OSHA compliant coaching, safety guards, hurricane and fireplace drill response trainings each 6 months, there could also be further controls wanted comparable to particular danger controls for catering operations and fireplace security measures for the outside open fireplace pizza furnace.

This supplementary data is invaluable in calculating the true danger publicity and attributing the proper danger stage to the client’s scenario.

Advantages to generative AI past extra worthwhile underwriting choices

In addition to aiding in additional worthwhile underwriting choices, these insights provide further worth as they educate new underwriters (in considerably lowered time) to know the info / pointers and danger insights. They enhance analytics / score accuracy by pulling all full, correct submission knowledge into CAT Fashions for every danger they usually cut back important churn between actuary /pricing / underwriting on danger data.

Please see beneath a recap abstract of the potential influence of Gen AI in underwriting:

In our latest AI for everybody perspective, we discuss how generative AI will rework work and reinvent enterprise. These are simply 3 ways in which insurance coverage underwriters can acquire insights from generative AI. Watch this area to see how generative AI will rework the insurance coverage business as an entire within the coming decade.

Should you’d like to debate in additional element, please attain out to me right here.

Disclaimer: This content material is offered for common data functions and isn’t supposed for use instead of session with our skilled advisors. Copyright© 2024 Accenture. All rights reserved. Accenture and its emblem are registered emblems of Accenture.

[ad_2]