[ad_1]

My basic principle concerning the web is nothing is correctly rated anymore as a result of there are such a lot of opinions on the market at present.1

The identical is true in the case of private finance. All the pieces might be over- or underrated.

Listed below are 3 monetary ideas I feel are overrated:

1. Eff-you cash. Having sufficient cash to do no matter you need everytime you need is the dream. Eff you cash sounds great…in principle.

The issue is most people who manage to pay for to do no matter they need every time they need don’t do this. The explanation they’ve eff you cash within the first place prevents them from ever utilizing it as such.

They develop into a slave to cash and energy. They work an excessive amount of, they journey on a regular basis, they combat on-line with different billionaires, they usually have horrible relationships with their spouses or kids.

The next comes from a New York Instances profile of Elon Musk:

He mentioned he had been working as much as 120 hours per week lately — echoing the explanation he cited in a latest public apology to an analyst whom he had berated. Within the interview, Mr. Musk mentioned he had not taken greater than per week off since 2001, when he was bedridden with malaria.

“There have been occasions once I didn’t depart the manufacturing unit for 3 or 4 days — days once I didn’t go outdoors,” he mentioned. “This has actually come on the expense of seeing my youngsters. And seeing buddies.”

The particular person with essentially the most eff you cash on the earth sounds depressing to me.

I don’t have billions of {dollars} however I simply took per week off work to spend time with my household on the lake. I’ve the time to educate my youngsters’ sports activities groups, go to their video games and participate at school features. I’m dwelling in dinner time each evening.

Cash is nice and all however it could actually develop into so all-consuming that it defeats the aim.

You don’t want hundreds of thousands of {dollars} to handle your time extra effectively. Having eff you cash doesn’t make a lot of a distinction in the event you don’t have your priorities straight.

2. A home is your greatest funding. Actual property can be an exquisite funding. You might have the inherent leverage concerned, the potential tax breaks and the long-term nature of the asset.

However for most individuals, proudly owning a house is only a place to stay that kind of retains up with inflation after accounting for all the prices concerned. Housing is as a lot a type of consumption as it’s a monetary asset.

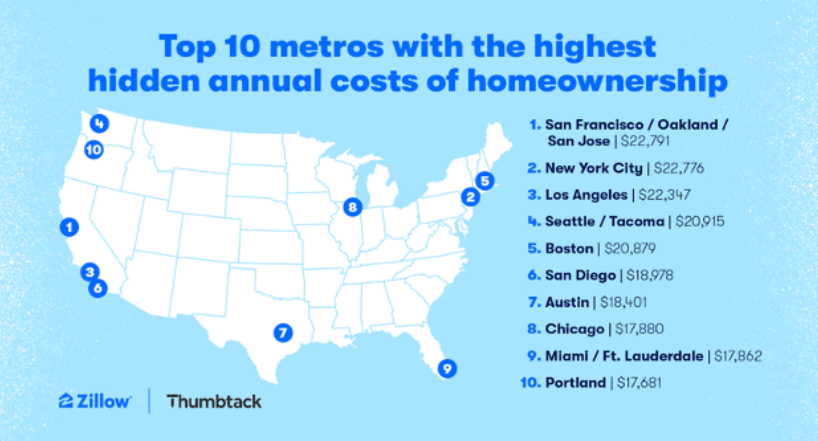

Zillow lately launched a brand new report on the hidden prices of homeownership. They estimate the common ancillary homeownership prices — utilities, insurance coverage, upkeep, property taxes, and many others. — to be greater than $14,100 a yr. That’s an extra $1,100 a month on prime of your mortgage.

And people numbers are even greater in most metro areas:

If you add in issues like garden care, furnishings and all the different stuff it’s important to purchase to replenish your home, these numbers are most likely on the low aspect.2

My level right here just isn’t that you must keep away from shopping for a home. A home continues to be a worthwhile funding for most individuals. However the largest return you get from proudly owning a house primarily comes from the psychic earnings you obtain from selecting your neighborhood and making a home your individual.

The previous few years have been a historic anomaly when it comes to home value good points.

Proudly owning a house just isn’t an important funding for the easy incontrovertible fact that most individuals do not know what their true fee of return is since nobody actually retains monitor of all the prices concerned within the course of.

3. Paying off your mortgage early. I perceive the psychological increase you may get from being debt-free. Some folks merely can’t stand owing different folks cash.

Nonetheless, I don’t get paying off your mortgage early.

Positive, it will get you out of month-to-month housing funds together with the mortgage curiosity however that freedom comes at a price.

First, you might have the chance price of that cash that might be invested elsewhere, not within the illiquid roof over your head. As soon as that cash is in your home you’ll be able to’t actually get it out until you borrow cash in opposition to your house or promote it.

Plus, a mortgage is tax-advantaged debt. Over a 30 yr lengthy interval inflation will eat into an enormous chunk of that debt. A home is already a reasonably first rate hedge in opposition to inflation however with a fixed-rate mortgage, all the higher.

And the leverage means that you can not put all your eggs into one basket in the case of your investments.

That cash additionally means much more to you if you end up younger and have the power to permit compound curiosity to do the heavy lifting for you within the inventory market.

I like the thought of getting your mortgage paid off by the point you retire. That makes all of the sense on the earth.

Paying it off early makes zero sense to me.

Additional Studying:

Why I Would possibly By no means Pay Off My Mortgage

1The opposite factor is the web has merely revealed there are at all times folks on the market with completely different tastes than you…and that’s OK. There’s a large distinction between “the very best” and “my favourite.”

2Plus you might have all the frictions concerned with shopping for and promoting a house like realtor charges, closing prices, value determinations, shifting bills, and many others.

[ad_2]