[ad_1]

A reader asks:

I’ve additionally at all times needed to do my very own “to not brag” so right here goes. I’m 33, I’ve $300k unfold between a Roth IRA, Roth 401k and taxable account all in VTI and VOO. I additionally personal my own residence and have $75k in money. I don’t actually perceive bonds apart from when charges go up, they go down in worth and vice versa. When TLT, the 20 yr bond ETF, it has crashed since charges began going up in 2022. Assuming we’re nearing the top of the speed improve cycle, even when charges keep greater for longer, why shouldn’t I take $50k and put it in TLT? If I maintain it for a couple of years, it stands to cause charges will likely be reduce sooner or later when inflation issues are behind us or the FED has to reply to a real recession. How excessive can charges really go from right here? This simply doesn’t appear long-term dangerous.

As at all times, threat is within the eye of the beholder.

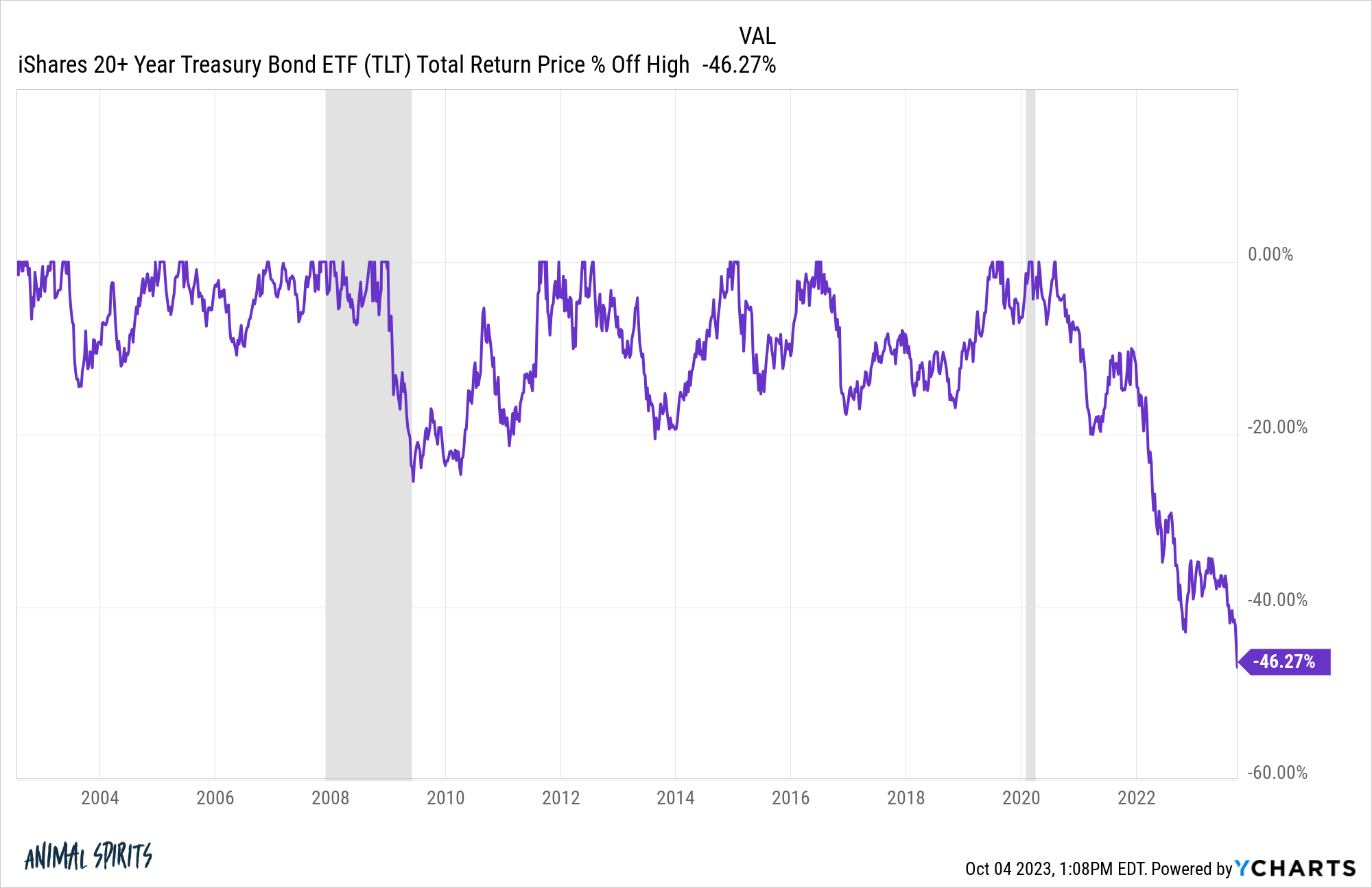

Lengthy-term bonds have crashed in a giant approach:

I depend seven separate corrections of 10% or worse for the reason that inception of this fund within the early-2000s. And rates of interest had been falling for a lot of this era.

The newest drawdown is a full-fledged crash.

One other approach of claiming that is long-term bond yields have gone up lots in a brief time frame.

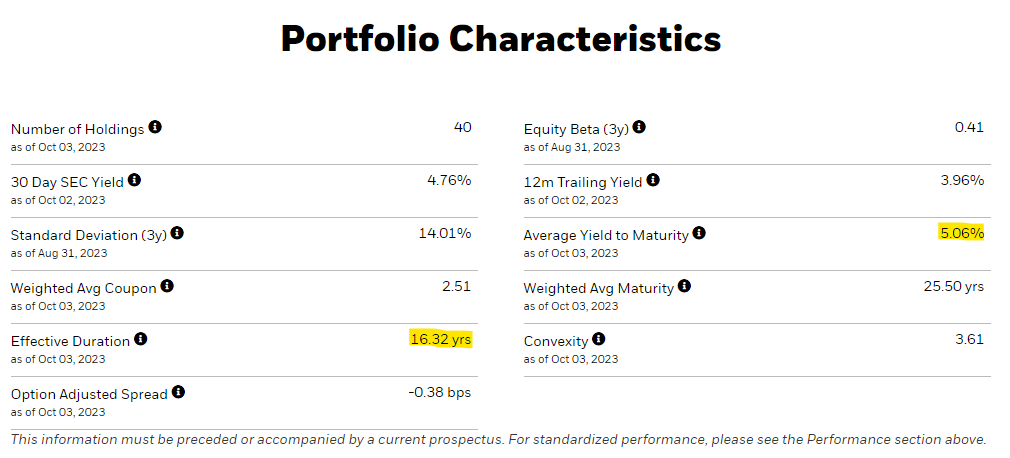

These are the portfolio traits of this long-term Treasury bond ETF:

I’ve highlighted two variables right here which are essential.

The common yield to maturity is now greater than 5%. On the depths of the pandemic, long-term charges had been round 1%.

It appeared unfathomable as little as 2-3 years in the past that buyers would be capable of lock in such excessive yields for such a very long time body. But right here we’re.

The opposite variable is the efficient period.

Bond period measures the sensitivity of bond costs to adjustments in rates of interest. For each 1% change in charges, you may anticipate bond costs to maneuver inversely by the extent of period.

For instance, if rates of interest on long-term bonds had been to fall 1%, you’ll anticipate TLT to extend by 16.3% or so. If charges rise 1%, TLT will fall 16.3%.

These are worth returns solely so you could possibly internet them out by the yield as effectively. With a median yield to maturity of 5%, there’s a a lot larger margin of security than there was within the latest previous.

If we get a recession or the Fed cuts charges or bond yields fall from greater demand or altering financial circumstances, TLT may make for an exquisite commerce.

It is smart yields ought to fall ultimately however I can’t assure they gained’t rise much more within the meantime.

What if yields rise to 7% earlier than dropping again all the way down to 3-4%? Are you able to sit by means of a 35% drawdown whilst you wait?

Or what occurs if yields don’t go anyplace for some time? Are you content material to spend money on TLT only for the yield and never the worth beneficial properties?

And what occurs when yields do start to drop? When do you get out? How a lot cash do you intend on making on this commerce?

I perceive the pondering behind this commerce but it surely’s not as simple because it sounds.

In his traditional Successful the Loser’s Sport, Charley Ellis highlights the work of Dr. Simon Ramo who made a vital remark concerning the two varieties of tennis gamers –professionals and amateurs.

Ellis explains:

Professionals win factors; Amateurs lose factors.

In skilled tennis the last word consequence is decided by the actions of the winner. Skilled tennis gamers stroke the ball arduous with laserlike precision by means of lengthy and sometimes thrilling rallies till one participant is ready to drive the ball simply out of attain or pressure the opposite participant to make an error. These splendid gamers seldom make errors.

Beginner tennis, Ramo discovered, is nearly solely completely different. The end result is decided by the loser. The ball is all too usually hit into the online or out of bounds, and double faults at service will not be unusual. Amateurs seldom beat their opponents however as an alternative beat themselves.

So how do you keep away from beating your self as an investor?

I like having guidelines in place to assist information my actions to attenuate errors.

I attempt to reduce errors by avoiding market timing, short-term buying and selling and investments that aren’t a match for my character and funding plan.

For example, I’ve by no means been a fan of proudly owning long-term treasuries. Sure they carried out phenomenally from 1980-2020 or so. And if we get double-digit yields on long-term bonds once more I’d be completely happy to personal some.

However I choose to take threat within the inventory market and hold the protected aspect of my portfolio comparatively boring. Which means brief period bonds and money. I already get sufficient volatility by proudly owning shares.

You possibly can earn excessive yields in brief and intermediate-term bonds proper now as effectively. These bonds will rally if charges fall, simply not as a lot as lengthy period bonds.

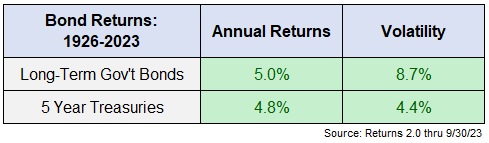

In case you take a look at the long-term returns in lengthy bonds, the case turns into far much less compelling exterior of a bond bull market or short-term commerce. These are the annual return numbers for long-term Treasuries and 5 yr Treasuries:

You get principally the identical return however with a lot greater volatility in lengthy bonds.

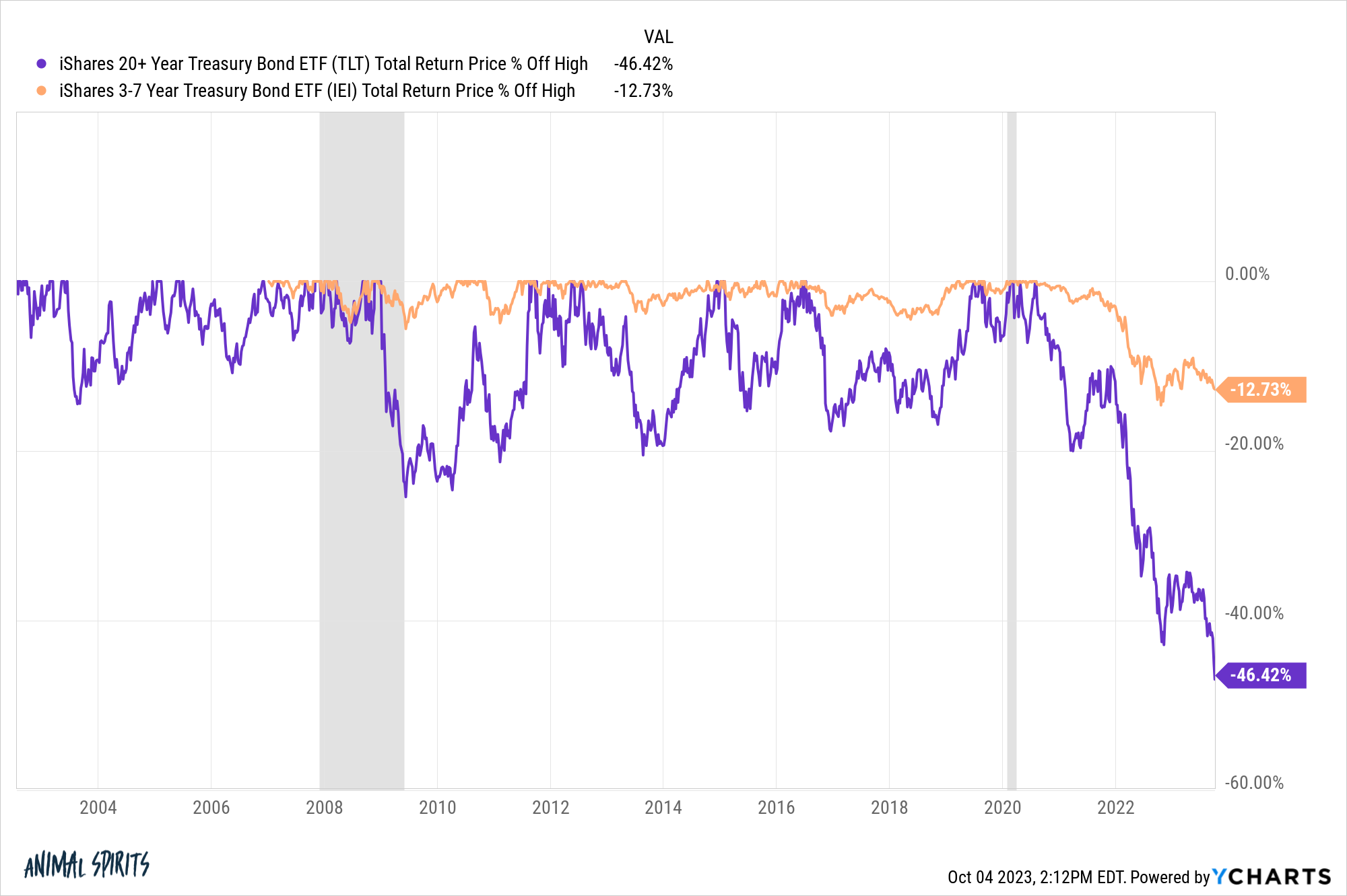

Simply take a look at the distinction within the drawdown profile of 20-30 yr bonds versus 3-7 yr bonds:

I’m not going to attempt to speak you out of a commerce so long as you go in along with your eyes large open. It’s solely potential lengthy bonds are establishing for an exquisite buying and selling alternative in the meanwhile.

However you actually need to nail the timing for a commerce like this to work.1

The excellent news is that you just don’t need to take part in each commerce or funding alternative. You possibly can choose your spots.

For many buyers, defining the stuff you gained’t spend money on is much extra essential than attempting to nail each single commerce.

We mentioned this query on this week’s Ask the Compound:

Nick Maggiulli joined me once more this week to speak about questions on greenback price averaging, locking in greater bond yields and the way a lot leverage is sufficient in your private steadiness sheet.

Additional Studying:

The Bond Bear Market & Asset Allocation

1Perhaps I’d change my thoughts if long-term charges ever get to 7-8%.

[ad_2]