[ad_1]

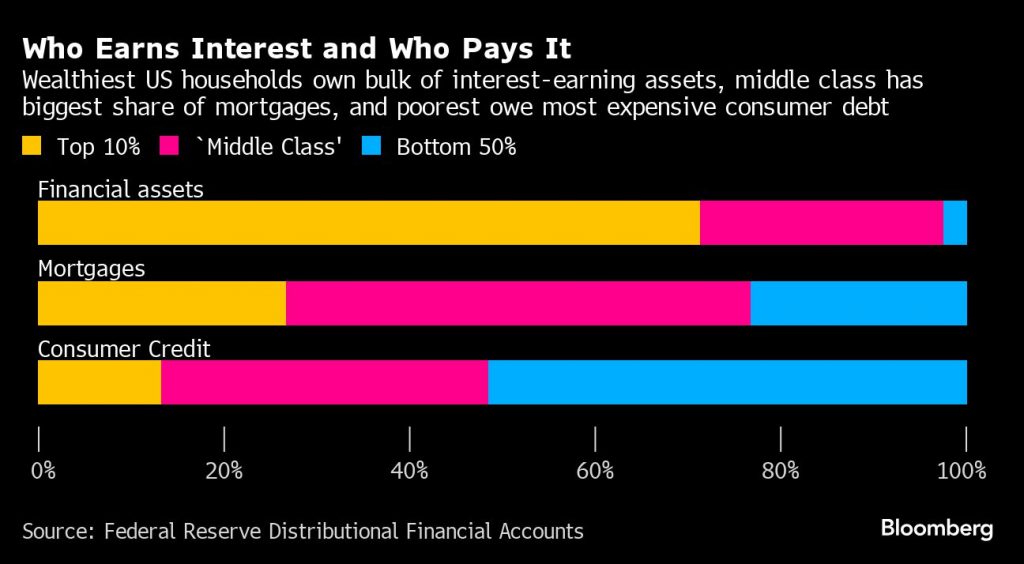

On the spending facet, curiosity prices rose quicker this time as a result of Individuals now have a bigger share of their money owed in shopper credit score, which is faster to reprice and saddles debtors with larger payments when charges go up. Mortgages, against this, are principally locked-in past the Fed’s attain.

As for curiosity earnings, one cause it’s lagged is that banks have been sluggish to cross on increased charges to depositors — they’ve come underneath hearth for that all around the world. And after about 15 years through which charges have been close to zero a lot of the time, savers might have gotten out of the behavior of shifting money between accounts seeking higher returns.

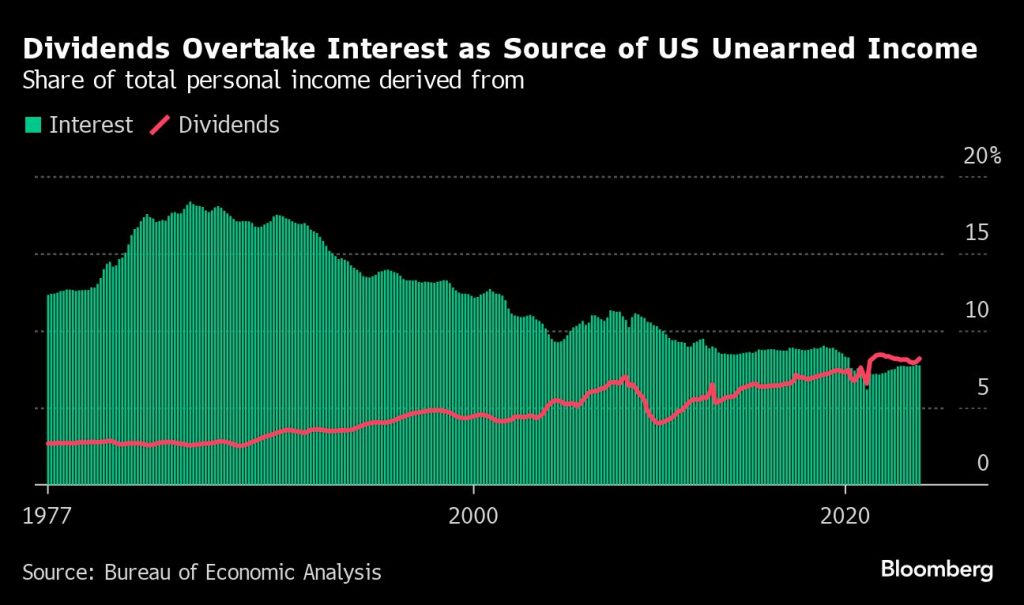

One other is that wealth has shifted out of the sort of holdings that pay curiosity, and into shares. Throughout the pandemic, for the primary time on file, dividends overtook curiosity funds as a supply of unearned earnings for Individuals.

To make sure, combination numbers not often inform the entire story, and within the case of curiosity earnings and funds they inform even much less of it than typical.

That’s as a result of the individuals who earn extra when charges go up are typically not the identical individuals who face larger payments. Possession of interest-earning property skews towards the wealthiest, whereas Individuals with the costliest sorts of debt usually tend to be decrease earners.

In addition to widening inequality, that distribution has penalties for the financial affect of charge will increase.

Put merely, the payouts are likely to go to savers who’re much less possible to offer the economic system a lift by spending every additional greenback on items and providers. In contrast, the payments land on the doorsteps of households who in all probability would’ve used these {dollars} to purchase stuff — in the event that they didn’t now must spend them on servicing debt as a substitute.

Photograph: Adobe Inventory; Charts: Bloomberg

[ad_2]