[ad_1]

During the last couple of days, we’ve got seen a media storm about current financial institution failures and the way these failures might (or might not) sign upcoming financial institution runs and a disaster within the total monetary system. Is there any reality to this media blitz or is it simply extra run-of-the-mill concern mongering to spice up scores?

There is no such thing as a crystal ball in relation to these things and one can by no means be certain of an end result, however with that stated, let’s dive into the info and see what we are able to decide.

Historic Context of Financial institution Failures:

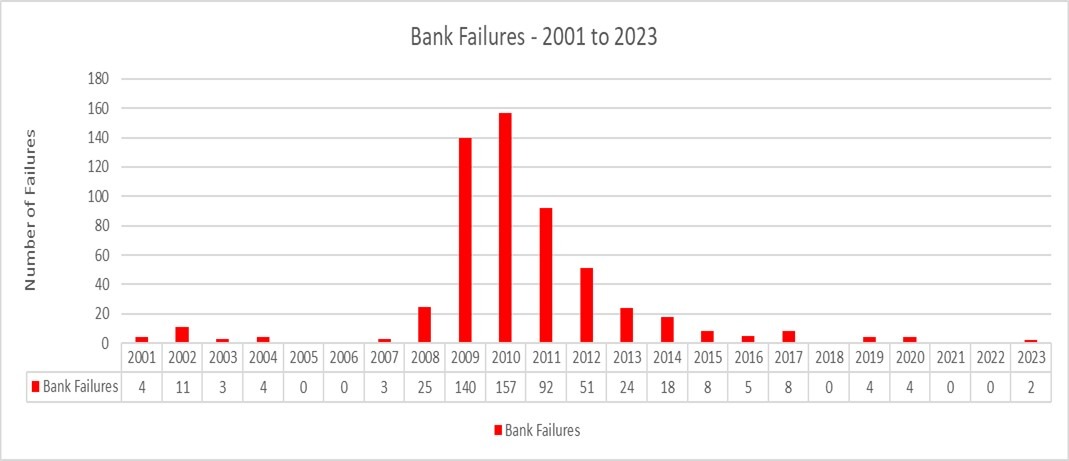

There is no such thing as a doubt that the media has latched onto the current financial institution failures and would have us consider that these occurrences are some type of never-before-seen phenomenon. The reality of the matter is that financial institution failures are fairly commonplace and occur nearly yearly. The truth is, in accordance with the FDIC, since 2001, there have solely been 5 years with no financial institution failures in any respect.[i] In Determine 1 under, you will notice a breakdown of these financial institution failures by yr.

Determine 1:

As you might have observed in Determine 1 above, the majority of the 563 financial institution failures from 2001 to 2023 came about throughout and straight after the Nice Monetary Disaster (GFC) between 2008 and 2012.[ii] Even when we eradicate these years from our evaluation, we nonetheless common simply over 5 financial institution failures per yr. Even in a yr like 2017, the place we skilled strong financial development and little or no monetary turmoil, there have been nonetheless eight financial institution failures.[iii]

Financial institution failures are usually not a brand new growth and the current media protection of the subject has no actual which means in and of itself.

Timing of Failures:

The present narrative is that “that is the start of a bigger banking disaster” and, if true, that could be a very scary prospect. All of us keep in mind the ache of the GFC and the lengthy street again from that extreme financial downturn. Nonetheless, if the financial institution disaster is brought on by systematic issues and is extra widespread, banks actually gained’t begin failing on a mass scale till after these systematic issues have change into obvious. The rationale for it’s because banks are huge, lumbering beasts and it takes a very long time for the systematic financial results to point out up on their stability sheet.

If we take a look at the various financial institution failures that occurred in the course of the GFC, we don’t see the failures occurring in 2007, earlier than the recession actually took maintain. The truth is, we don’t actually see a big uptick of failures till 2009. The technical recession in the course of the GFC came about from This autumn 2007 to Q3 2009, however the bulk of the failures occurred after the recession was truly over.[iv],[v]

From an funding standpoint, these financial institution failures actually began occurring after the technical bear market backside, which occurred on March 9th, 2009. If you happen to used financial institution failures as a knowledge level to make your funding choices, you’ll have missed out on one of many steepest bull market recoveries in historical past, because the S&P 500 Complete Return rose over 70% within the subsequent 12 months.[vi]

If we actually begin to see an uptick in financial institution failures, it gained’t sign the start of a recession, however fairly that we’re doubtless many of the means by means of one. In different phrases, financial institution failures are way more of a lagging indicator than a main indicator.

Systematic or Mismanaged:

The important thing to figuring out whether or not there are a slew of financial institution failures across the nook, or if that is simply one other typical yr, is to determine if the issues confronted by Silvergate, Signature, and Silicon Valley Financial institution (SVB) had been systematic and can have an effect on different banks in mass or if these points had been merely the outcomes of mismanagement. Let’s take a deeper dive.

You will need to notice that it’s nonetheless very early within the financial institution liquidation course of. Consequently, not all the particulars associated to those failures are public information but. This evaluation relies on probably the most present info accessible to our staff.

Silvergate Financial institution:

Silvergate is a really attention-grabbing financial institution, because it centered its companies totally on crypto and crypto-related companies. The truth is, certainly one of Silvergate’s largest purchasers was FTX, which is now bankrupt and continues to be below investigation for fraud. Because the finish of 2021, most crypto tokens have fallen in worth by 60% to 70%. This devaluation harm a big majority of Silvergate’s clientele and, finally, this weak spot bled by means of and confirmed itself on Silvergate’s stability sheet. Then, on March 8th of 2023, Silvergate primarily noticed the writing on the wall and commenced a voluntary discontinuation of enterprise with a plan to return all deposits to its depositors.[vii] Silvergate is an ideal instance of the way it takes time for issues to actually begin to present on a financial institution’s stability sheets. The crypto rout started in late 2021, nevertheless it took about 14 months earlier than Silvergate introduced that it will be shutting its doorways.

In our evaluation, it wasn’t broad systematic issues or extreme mismanagement of the enterprise that led to Silvergate’s demise, however extra of a problem with their enterprise technique. They hitched their wagon to the crypto horse and that horse didn’t make it very far. You may argue that, if it wasn’t for the FTX fraud, Silvergate might have continued operations, however hindsight is at all times 20/20.

The actual query at hand is: are the underlying components that brought on the Silvergate failure contagious, and can that have an effect on a broader set of banks? Put merely, no. there might be another banks effected by the issues within the crypto area, however it is going to be a slim sliver of the general banking trade. Which leads properly into the following evaluation…

Signature Financial institution:

Signature, like Silvergate, was one of many few banks that serviced crypto and digital asset clientele. They launched their digital asset companies in 2017, once they had roughly $33 billion in property. Since that point, they’ve greater than tripled their complete property to over $100 billion.[viii] Though Signature claimed, in December of 2022, that deposits from operators within the digital asset area solely accounted for 23% of complete deposits (which continues to be very excessive), it’s exhausting to think about that quantity wasn’t far increased.[ix] And, like Silvergate, they’d a whole lot of involvement with FTX, which broken their model.

From an asset perspective, Signature’s stability sheet was pretty sturdy, as they carried lower than 10% of held to maturity securities, and most of their property had been brief time period in nature and really liquid.[x] Nonetheless, nearly 90% of the deposits held by signature had been above the FDIC limits, which means they had been successfully uninsured.[xi] That is primarily as a consequence of the truth that digital property, and the extra speculative kinds of corporations that Signature served, had nowhere else to place their cash. In different phrases, they successfully put all their eggs in a single basket.

In the end, Signature Financial institution, though way more diversified than Silvergate, served a extra speculative area of interest of the market. When SVB failed (which we’ll cowl subsequent), Signature’s slim buyer base received antsy and withdrew greater than 20% of their complete deposits in a single day from the struggling financial institution. It was the mix of the shoppers that Signature selected to serve and the truth that this specific clientele didn’t have many choices for the place to retailer their cash that led to the financial institution run and, finally, Signature’s failure.

Give it some thought this fashion, should you had been solely ready to make use of a single financial institution in your complete life financial savings after which a financial institution similar to it failed, would you let the cash sit or would you get it out as quick as humanely attainable?

In the meantime, there may be continued hypothesis that the financial institution didn’t truly must be shuttered, however was closed to ship a message by regulators who wished to point out that they’re severe about regulating the digital area. We’ll doubtless by no means know.

Identical to with Silvergate, our evaluation is that the failure of Signature was not as a consequence of systematic issues, however fairly a strategic resolution that didn’t play out how the financial institution had hoped. The technique benefited them enormously from 2017 to 2022, however grew to become their undoing during the last 14 months. That’s to not say that asset pricing, rates of interest, and the Internet Curiosity Margin didn’t additionally play a task, we simply don’t suppose that these components performed as giant of a task because the media would have us consider.

Silicon Valley Financial institution (SVB):

Now, we get to the most important (and sure most essential from a macro perspective) of the three current financial institution failures: Silicon Valley Financial institution (extra generally generally known as SVB).

Silicon Valley Financial institution has been round since 1983 and was a monetary companies staple of the tech trade.[xii] In comparison with Signature and Silvergate, SVB was a behemoth with a bit of over $200 billion in complete property, making it the 16th (or thereabout relying on the supply) largest financial institution in the USA.[xiii] Though these are very giant numbers, it was by no stretch of the creativeness one of many largest or most influential banks within the US. The truth is, SVB was thought of a “mid-sized” financial institution. For comparability, the most important financial institution within the US is JP Morgan Chase, which holds roughly $3.7 trillion in complete property.[xiv] That’s not a typo, “trillion” with a T.

SVB has centered its enterprise on enterprise capitalists, start-ups, and the tech trade as a complete. Even its web site, which has now been taken over by the FDIC, focuses its language and content material nearly totally round these teams, as proven in Determine 2 under.

Determine 2:

This extremely centered technique deployed by SVB had been very profitable previously, particularly over the previous couple of years. For instance, SVB nearly doubled its complete property in 2020, rising from roughly $115 billion to over $200 billion in a single yr (does this appear paying homage to Silvergate?).[xv] That’s merely extraordinary development for a financial institution of this dimension. The truth is, it’s mainly unprecedented. This stage of development was primarily because of the COVID-era tech bubble, as start-ups had been popping out of the woodwork. The issue is that this space of tech would show to be fairly unstable, particularly because the world started to return to regular. The crypto and digital asset increase slowed to a crawl and all these small tech corporations noticed their income merely dry up, in the event that they even had it within the first place. Sadly, these had been the purchasers of SVB and, accordingly, the financial institution skilled nearly zero development in 2022.[xvi] That’s fairly a change from its earlier years and one thing that I don’t suppose administration was anticipating. The truth that this area skilled a big slowdown meant that, as a substitute of including to the funds held at SVB, they had been pulling funds out to fulfill payroll and expense obligations. In spite of everything, most of these corporations have a really excessive burn charge.

The immense development skilled by SVB gave administration an elevated urge for food for threat, which will be seen on the financial institution’s stability sheet. On the finish of 2022, roughly 43% of SVB’s property had been labeled as held-to-maturity securities.[xvii] Held-to-maturity (HTM) securities are usually not meant to promote. As their identify suggests, they’re meant to carry till they mature, at which level they’d pay again the unique precept paid. When an HTM safety is bought to cowl withdrawals, it requires all different HTM securities in that class to be marked all the way down to the latest market value, primarily reclassifying them as “accessible on the market”. Put merely, SVB was so assured of their means to continue to grow and gathering extra deposits that they bought securities that paid them a better return, however might have been extra unstable. That is what’s known as a “attain for yield” and it hardly ever ends properly. For comparability, JP Morgan Chase holds roughly 11% of their property in HTM securities.[xviii]

Because the withdrawals continued to pile up, SVB had to determine tips on how to return cash to its depositors, so on March 8th of 2023, they determined to aim a capital elevate within the quantity of $1.8 billion.[xix] That is the place every part started to go downhill, quick. There may be a whole lot of hypothesis as to the occasions of the next few days, however the frequent narrative is that the message conveyed by the potential capital elevate panicked depositors. What occurs subsequent could be very unlikely to happen in a financial institution with a extra diversified depositor base, however on March 9th of 2023, there have been $42 billion in tried withdrawals that compelled SVB to liquidate a piece of their HTM securities and left them with a money shortfall of $958 million.[xx] It was at this level that regulators stepped in and turned the financial institution over to the FDIC.

What Brought on the Run on SVB?

As we’ve got outlined above, SVB had a really concentrated depositor base that was primarily comprised of tech startups and enterprise capitalists. These depositors are a tight-knit group. As well as, it wasn’t simply the companies themselves that had deposits at SVB, it was their workers, pals, and relations as properly. These depositors had been additionally fairly rich and, in lots of instances, had deposits properly in extra of the $250,000 FDIC insurance coverage restrict. The truth is, about 93% of SVB deposits had been in extra of the FDIC restrict (once more, does this remind you of one other financial institution…trace, trace).[xxi] When the capital elevate was introduced, it spooked these companies, which held a lot cash with SVB. Consequently, these companies reverberated the message to withdraw funds from SVB to everybody of their group, together with workers, pals, and relations. It seems that message was obtained, leading to huge withdrawals occurring in a single day.

Systematic or Mismanagement?

Primarily based on our evaluation, what occurred to SVB just isn’t a scientific drawback, however, once more, a method and administration drawback. SVB made a acutely aware resolution to take a excessive stage of threat on each the back and front finish. They catered to a really slim group of depositors and took extra threat reaching for yield on the funding aspect. These choices paid off enormously just some years in the past, however finally led to the demise of SVB. Rates of interest did play their half within the undoing of SVB, however finally the results of rising charges might have been mitigated with correct threat administration, however merely weren’t. The mantra of Silicon Valley is “develop or die” and, in SVB’s case, they had been capable of attain each in a really brief period of time.

Financial institution Failures – The Macro Image:

In our view, the financial institution failures are usually not systematic, however there are systematic variables (rates of interest) at play that contributed to those failures, which is why everyone seems to be so involved a few potential contagion. These banks had been all mismanaged (pretty clearly) and the failures might have simply been averted.

Will there be extra financial institution failures? In fact there’ll. As we talked about beforehand, banks fail nearly yearly and this yr might be no totally different. Rising rates of interest will expose banks which have been mis-managed and these banks will definitely face problem and perhaps a number of extra will fail. Financial institution runs, in and of themselves, generally is a self-fulfilling prophecy and for these mismanaged banks, it might be a tricky storm to climate. Though that is tough for depositors and workers of those establishments, it isn’t essentially a nasty factor for the long-term well being of the general banking trade. Sometimes, the herd have to be culled to make it stronger and extra agile.

Within the meantime, people and the media are going to proceed the witch hunt to seek out the following SVB and do every part they’ll to make parallels to 2008, Bear Stearns, and Lehman Brothers. The fact is, nevertheless, that banks, as an trade, are about as sturdy as they’ve ever been. Making a real contagion most unlikely.

A Observe on Coverage:

US regulators have opened up mortgage amenities that enable banks to borrow cash towards their HTM securities at par worth, so they don’t have to promote them. It is a harmful recreation as a result of it might incentivize extra dangerous conduct by banks in the event that they consider that they may by no means must promote HTM securities. With that stated, within the brief time period, it will doubtless instill some confidence and assist forestall potential financial institution runs, nevertheless it have to be handled fairly delicately. We’ll proceed to observe the banking trade for brand spanking new developments.

Moreover, regulators have determined to completely reimburse all depositors at SVB and Signature Financial institution, which is nice for depositors, however doubtlessly very dangerous for small- and mid-sized banks. The choice to make depositors complete on this state of affairs relies on an arbitrary measure of the financial institution being “systematically essential”. Put extra bluntly, banks which are decided NOT to be systematically essential is not going to obtain this identical remedy. Within the brief time period, it’s attainable that it will induce extra financial institution runs on small banks. In the long term, it extremely incentivizes depositors to maintain their cash on the largest banks. If this line of resolution making continues, it gained’t be lengthy till the massive banks get larger and the small banks get smaller or just go away.

Give it some thought this fashion, when you’ve got a number of million bucks or extra, are you going to place that cash in a big financial institution, through which the federal government will assure each penny, or The Oakwood Financial institution of Texas?

What it Means for Buyers:

The media has actually latched onto these financial institution failures and made them seem very horrifying. Why they by no means publicize different financial institution failures is past us, however they’ve accomplished an exceptional job of concern mongering based mostly on current occasions. Nonetheless, media blathering doesn’t make these failures any extra of a scientific drawback. Banks, on the whole, are in fairly fine condition. Within the brief time period, you by no means know what inventory and bond markets will do, however it’s doubtless that financials and regional banks will expertise a better stage of volatility than different areas of the market (on each the up and draw back). In the long run, the economic system retains chugging alongside and, even when we’ve got a recession within the close to time period, that’s already priced into markets.

When you have a well-diversified portfolio and strong monetary plan, then now could be the time for endurance and self-discipline, not rash resolution making based mostly on the latest headlines. This too shall cross.

[ad_2]