[ad_1]

Once we consider utilization administration (e.g., prior authorizations, step edits), we frequently suppose payers solely use these for increased price branded merchandise together with biologics. Generic medicine ought to have low price sharing and restricted utilization administration. One query, nevertheless, is whether or not payers’ utilization administration practices for biosimilars mirror these of biologic merchandise, or small-molecule generics, or someplace in between.

A paper by Yu et al. (2023) goals to reply this query. The authors used information from the Tufts Medical Middle Specialty Drug Proof and Protection (SPEC) database overlaying 19 commercially-available biosimilars akin to 7 reference merchandise. These merchandise had been used for 28 distinctive indications. The authors discover that:

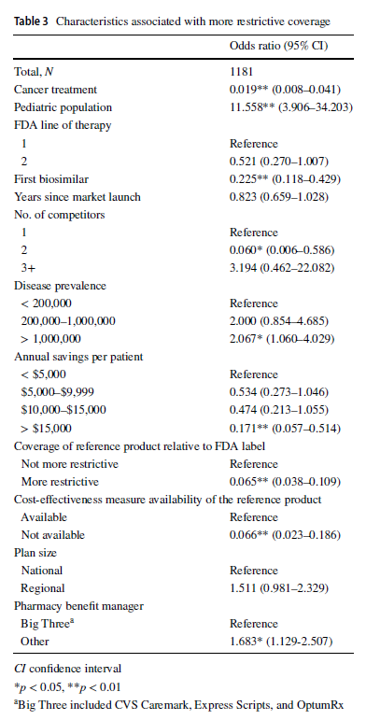

In contrast with reference merchandise, well being plans imposed protection exclusions or step remedy restrictions on biosimilars in 229 (19.4%) selections. Plans had been extra prone to limit biosimilar protection for the pediatric inhabitants (odds ratio [OR] 11.558, 95% confidence interval [CI] 3.906–34.203), in ailments with US prevalence increased than 1,000,000 (OR 2.067, 95% CI 1.060–4.029), and if the plan didn’t contract with one of many three main pharmacy profit managers (OR 1.683, 95% CI 1.129–2.507). In contrast with the reference product, plans had been much less prone to impose restrictions on the biosimilar–indication pairs if the biosimilar was indicated for most cancers remedies (OR 0.019, 95% CI 0.008–0.041), if the product was the primary biosimilar (OR 0.225, 95% CI 0.118–0.429), if the biosimilar had two opponents (reference product included; OR 0.060, 95% CI 0.006–0.586), if the biosimilar might generate annual listing worth financial savings of greater than $15,000 per affected person (OR 0.171, 95% CI 0.057–0.514), if the biosimilar’s reference product was restricted by the plan (OR 0.065, 95% CI 0.038–0.109), or if a cost-effectiveness measure was not out there (OR 0.066, 95% CI 0.023–0.186).

One fascinating discovering was that giant PBMs truly had much less restrictive insurance policies over biosimilars. Why?

… it has been posited that the bargaining energy of bigger PBMs could also be so important that biosimilar producers might generally increase listing costs, and therefore rebates, to acquire a spot on the formularies of huge PBMs. This would depart smaller PBMs with increased listing costs however

smaller rebates on account of their comparatively smaller bargaining energy, wherein case the biosimilars convey much less worth to them.

You possibly can learn the complete paper right here.

[ad_2]