[ad_1]

Sheila and Marcus personal a public relations and advertising enterprise with 54 workers. They wish to foster a model that appears “hip,” even when which means hiring some nice individuals who might not stick round lengthy. From the beginning of their enterprise, they’ve created an surroundings the place advantages play an important position. Periodically they ask themselves, “Does it pay to carry on new services and products or do these largely go unused? How can we all know that our advantages are pretty priced? Do our workers get good service from our chosen suppliers?”

Justin is a senior govt within the firm. He has a variety of obligations for the enterprise, together with operations, payroll, HR, and advantages administration. Along with his a number of roles, he’s stretched skinny, however he has seen lately that new workers complain about scholar loans and battle with life-work stability. He wonders if new varieties of advantages and companies may assist them and enhance their work satisfaction. He additionally wonders if new profit choices might assist them appeal to gig staff.

Megan is a latest graduate, simply employed as an affiliate account consultant. She is new to the working world, and he or she doesn’t perceive advantages but. What she does perceive, she discovered utilizing YouTube tutorials, not the corporate’s advantages information. In her first week, as she’s making an attempt to additionally be taught her job, she is drowning in a sea of insurance coverage phrases and choices. She makes some elections primarily based on a pal’s suggestion and he or she determines that she’ll attempt to be taught extra subsequent yr. Essentially the most irritating a part of the method is that enrolling doesn’t simply occur on one system. She should name some voluntary advantages suppliers, equivalent to her pet insurance coverage, and stroll by means of their steps individually.

To grasp at present’s Group & Voluntary market alternatives, it’s useful to look by means of the eyes of all three of those enterprise varieties — house owners, execs, and workers. In Majesco’s SMB thought management report, Resiliency in Occasions of Change: Rethinking Insurance coverage to Assist SMBs Thrive, we have a look at SMB priorities, altering demographics, and insurance coverage challenges which are impacting the business at massive. By SMB and worker pressures and priorities, we are able to additionally decide the place expertise investments are greatest utilized in an effort to create resiliency and profitability.

Placing the digital foot ahead.

As Millennials and Gen Z SMBs proceed to develop in proudly owning companies, they are going to more and more problem insurers as a result of they view and worth issues otherwise than the older technology. However extra importantly, they’re extremely digital in how they do enterprise. They anticipate and demand digital capabilities for his or her enterprise administration and worker advantages.

They need companies, protection, and interactions which are accessible to them each time they need them, and nevertheless they want to have interaction. Including worth to conventional merchandise and creating new ones will likely be essential to fulfill the distinctive wants of this technology of SMBs.

Any firm keen on recruiting high-quality expertise can even be confronted with making their surroundings match the lives and existence of their workers. New workers particularly will likely be envisioning how their work will help their life. Service should be easy and customized. Merchandise should be clear. The worth should be apparent.

Which group & voluntary merchandise do SMBs at the moment supply, if they provide something in any respect?

Majesco’s survey discovered that lower than half of Gen Z and Millennial (38%) and Gen X and Boomer (43%) SMB house owners supply voluntary advantages — a low quantity given the battle for expertise. Amongst those that do, conventional advantages of well being, imaginative and prescient, life, incapacity earnings, and dental are the highest merchandise provided, starting from 52% to 89% seen in Determine 1. Accident insurance coverage, vital sickness, and long-term care create a second tier ranging between 30% and 38%.

After these two tiers, all different advantages drop off precipitously within the Gen X and Boomer phase however stay comparatively sturdy within the Gen Z and Millennial phase. Specifically, P&C insurance coverage choices, authorized companies, and scholar mortgage help all are comparatively new voluntary profit choices. These outcomes spotlight that Gen Z and Millennial SMB house owners look like extra in tune with the altering wants and expectations of at present’s workers – particularly the youthful technology – and the worth of providing newer and progressive profit choices to draw and hold workers. This highlights development alternatives for insurers who can supply advantages that meet a extra various worker base with altering wants and expectations.

Determine 1: Voluntary advantages provided

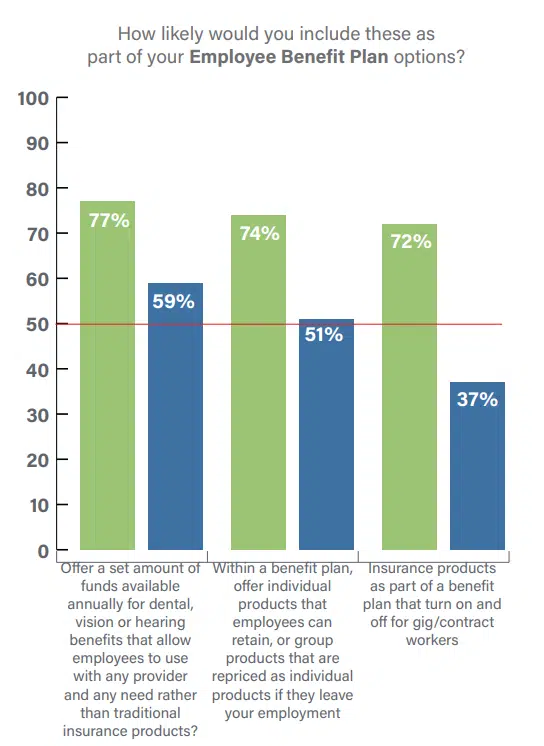

After we requested SMB house owners about dental, imaginative and prescient, and listening to advantages and the need for flexibility and ease, there was a powerful curiosity with each generations at 77% and 59%, as seen in Determine 2. This idea would supply workers the higher latitude to spend a set pool of funds on no matter procedures and with no matter suppliers they select, moderately than being restricted to a particular community or restricted procedures lined.

Likewise, profit merchandise which are provided as particular person/worksite merchandise, or as group merchandise that may be repriced and ported for workers to take with them in the event that they go away employment are of excessive curiosity from Gen Z and Millennial SMBs (74%). They acknowledge their technology’s tendency to see employment as fluid. Their response is to hunt advantages that can appeal to expertise by becoming with a prospect’s imaginative and prescient of their future — as a substitute of assuming that they are going to stick with the corporate long-term. And whereas curiosity is decrease with Gen X and Boomer SMBs (51%), there may be nonetheless sturdy market potential. More and more, employers and brokers are in search of profit plans that supply a broader vary of merchandise that meet the altering wants of their various worker base – highlighting a possibility for insurers to suppose past conventional profit choices.

Gen Z and Millennial SMBs are additionally keen on on-demand advantages that may be turned on and off with engagements as a Gig or contract employee. Given the sturdy use of this worker sort, it isn’t shocking they might search progressive profit plans to draw this employee phase. Whereas Gen X and Boomers usually are not as and use contract/gig staff much less, their acceleration in the usage of this worker phase over the past yr might alter their views on providing on-demand advantages sooner or later.

Determine 2: Curiosity in providing new worker profit plan choices

Group and voluntary advantages are important instruments for attracting and retaining the expertise that SMBs want, notably given the low unemployment charges, fluidity of youthful generations, and the expansion within the Gig market. By serving to to guard their monetary safety, employers are serving to workers to stay extra targeted, motivated, and productive. It follows that any new or progressive choices that improve that safety can be development alternatives for insurers to supply SMBs.

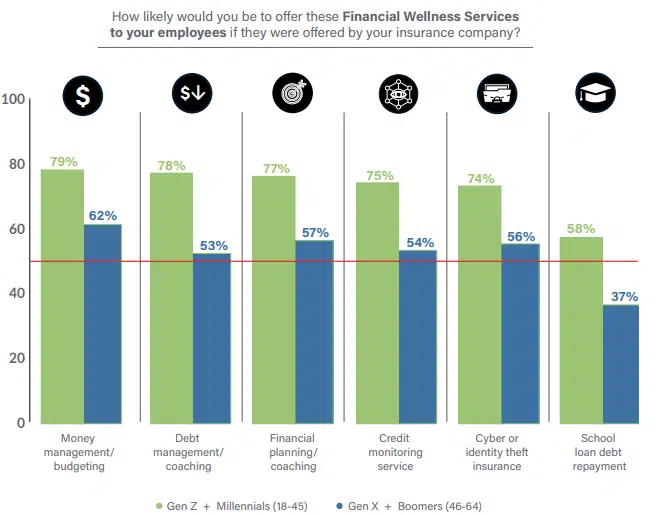

For SMB workers, monetary wellness is a rising concern.Majescofound that whereas Gen X and Boomer SMBs exceed 50% curiosity in 5 of six potential monetary wellness companies choices, Gen Z and Millennials present considerably greater curiosity, from 74% to 79%, as highlighted in Determine 3. As well as, Gen Z and Millennials present sturdy curiosity (58%) in providing scholar mortgage debt compensation help, an possibility that could be much more enticing after the June 30, 2023, Supreme Courtroom choice concerning scholar mortgage forgiveness.

Private experiences and views of retirement monetary viability are probably influencing these gaps. Gen X and Boomers have accrued extra monetary administration skills and confidence over time and have reached or are approaching Social Safety eligibility. In distinction, the youthful technology struggles to purchase properties and has issues about whether or not Social Safety will likely be accessible once they retire. Insurers who may also help employers handle these points have a possibility to construct belief and loyalty.

Determine 3: Curiosity in providing monetary wellness companies to workers

Knowledge transformation pays off in improved pricing and elevated gross sales

With inflation and funds/profitability the highest two issues going through all SMBs, it’s vital for insurers to reveal transparency, equity, and accuracy of their pricing. Utilizing new, progressive information sources that may personalize the pricing can obtain this, supplied SMBs are comfy with information sharing. When marketed correctly, insurers ought to see a rise in gross sales by means of clear and aggressive pricing that gives its personal justifications.

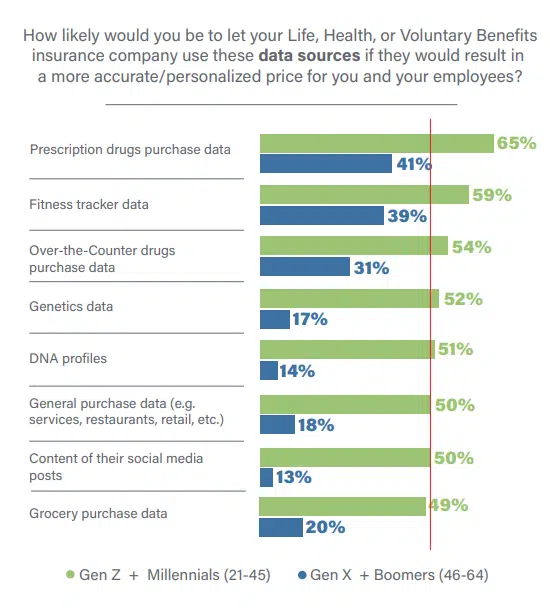

Gen X and Millennial SMBs are overwhelmingly keen on the usage of new information sources for extra correct, customized pricing as seen in Determine 4 — which given the curiosity in particular person and transportable merchandise is vital. Between 49% and 65% of Gen Z and Millennial SMBs are keen on their use for all times, well being, and voluntary advantages. In distinction, Gen X and Boomers are much less comfy total, with prescription (41%) or over-the-counter (31%) drug buy information and health tracker information (39%) representing probably the most curiosity. Curiosity in all different information sources drops dramatically, with a low of 13% for content material from social media posts and 14% for DNA profiles.

Determine 4: Curiosity in new information sources for all times/medical insurance and voluntary advantages pricing

As soon as once more, the massive disparities in expectations between the generational segments require insurers to rethink their merchandise, information sources, and pricing approaches to higher meet the wants and calls for of diverging expectations. Subsequent-gen underwriting and coverage programs will likely be required to successfully handle these calls for.

Worth-added companies present sturdy and rising attraction for SMB house owners

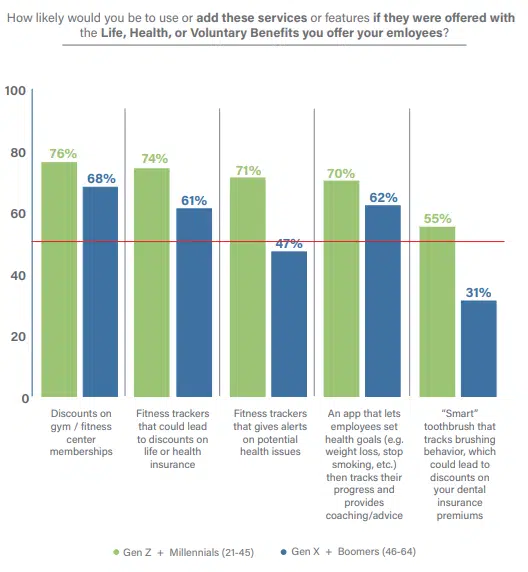

A key technique for insurers to handle SMBs’ issues about inflation, funds, and expertise acquisition is to extend the worth of the merchandise they provide. To take action, insurers ought to bundle, or supply for a value, companies that reach the worth of the danger product/coverage, equivalent to incomes factors for wellness that can be utilized to purchase issues, annual monetary planning assessments, roadside help, and extra.

Each SMB technology segments are extremely keen on value-added companies as seen in Determine 5. Curiously, 61% of Gen X and Boomers can be keen on providing workers health trackers that might result in reductions on life or medical insurance.

Determine 5: Curiosity in value-added companies with life/medical insurance and voluntary advantages

Making ready to develop into newer channels whereas giving nice service by means of established channels.

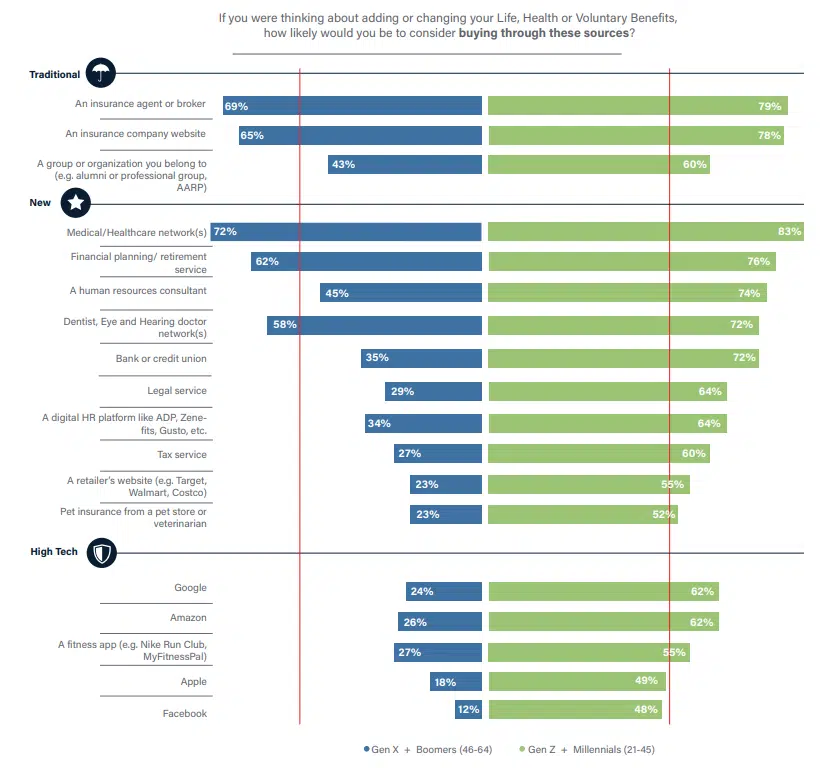

Conventional distribution channels for purchasing life, well being, and voluntary advantages – insurance coverage firm web sites and brokers/brokers – proceed to be among the many hottest choices in each generational segments, however they’re eclipsed for the primary spot by medical/healthcare networks (83%, 72%) as seen in Determine 6. The subsequent group with sturdy curiosity is monetary planning/retirement service (76%, 62%) and dentist, eye, and listening to physician networks (72%, 58%). Given the character of SMBs being very localized, the curiosity in medical or healthcare networks throughout the group or state isn’t a surprise and opens up new partnership choices for insurers to think about.

After these 5 channels, Gen X and Boomer SMBs present considerably much less curiosity in any of the opposite choices. In distinction, Gen Z and Millennials are keen on all the channel choices, even two of the GAFA corporations (Apple and Fb) that are just below 50%. Some analysts are predicting Apple will enter the medical insurance market in 2024, leveraging wealthy health and well being information gathered from hundreds of thousands of Apple Watch customers,[i] which can instantly align with their want for customized insurance coverage utilizing information from health trackers.

Determine 6: Curiosity in channel choices for all times/medical insurance and voluntary advantages

There’s a hurdle, nevertheless, in practically all of those circumstances. Quickly, many services and products will likely be bought and consumed by means of different, non-traditional channels. How are group & voluntary insurers going to arrange to promote and associate with organizations that may carry them further enterprise? How will they deal with not solely transaction information however the circulation of customized information backwards and forwards from corporations, past shopping for to serving and claims, by means of channels and into their present programs? How will they adapt their expertise to these companions for a constant one for consumers?

Can group & voluntary insurers prioritize updates to their information frameworks, in addition to enhance their digital service by means of cloud-based core programs? These are questions of fast significance as SMBs rapidly develop adept at finding and carrying progressive advantages and companies.

The SMB market alternative is rising bigger annually. SMBs make use of practically 50% of all US workers. Is your group prepared for the brand new improvements in group & voluntary services and products? Let Majesco show you how to create an SMB-focused tech technique that features all the options and capabilities your group must innovate.

For extra details about SMB group & voluntary traits or to search out out extra about SMB wants, make sure to learn Resiliency in Occasions of Change: Rethinking Insurance coverage to Assist SMBs Thrive after which dig into element particularly on present gaps in group & voluntary advantages with Bridging the Buyer Expectation Hole: Group & Voluntary Advantages.

[i] Collins, Barry, “Apple Will Launch Well being Insurance coverage In 2024, Says Analyst,” Forbes, October 18, 2022, https://www.forbes.com/websites/barrycollins/2022/10/18/apple-will-launch-health-insurance–in-2o24-says-analyst/amp/

[ad_2]