[ad_1]

The economic system has been by means of lots over the previous couple of years. We turned it off and turned it again on once more like we had been restarting a online game.

A mix of fiscal stimulus and provide chain disruptions led to an inflationary spike not seen in over 4 a long time. All of the containers caught within the ports of Los Angeles wreaked havoc on many consumer-facing corporations. Semiconductors had been in brief provide. Used automotive costs went by means of the roof.

Amidst all the chaos, Russia invaded Ukraine, which despatched vitality and commodity costs vertical. To sluggish all of this down the Federal Reserve undertook a historic improve in rates of interest; mainly straight up for the final yr and counting. That prompted the housing market, not less than the prevailing one, to all however freeze over. It additionally prompted a number of monetary establishments to mismanage their rate of interest danger and led to a few of the greatest financial institution runs this nation has ever seen.

Rising rates of interest destroyed any urge for food for risk-taking, with tech being on the epicenter of the passion unwind. Enterprise funding dried up, IPOs floor to a halt, and even mega-cap tech corporations had been pressured to do mass layoffs. Alongside the best way, the S&P 500 fell 25%, and the Nasdaq-100 misplaced greater than a 3rd of its worth.

The $3 trillion workplace actual property market goes to expertise some ache over the following few years with occupancies down and borrowing prices up. And the cherry on high of this disgusting sundae is the looming contraction in credit score.

How a lot can we take?

I don’t know the place the tipping level is, however the obvious reply to this query is much more than anybody thought. Issues aren’t good, however we recovered all the roles misplaced in the course of the pandemic, the unemployment charge remains to be close to document lows, and inflation goes in the proper path.

And this week we heard from banks that the buyer remains to be okay. We received’t study the total influence of the financial institution run till subsequent quarter, however no matter that, it’s unbelievable that People have been so resilient given all of the headwinds talked about above. Even had we not seen the financial institution runs, there nonetheless would have been questions in regards to the sturdiness of shopper spending. We bought solutions in latest earnings calls from corporations like Financial institution of America and American Categorical.

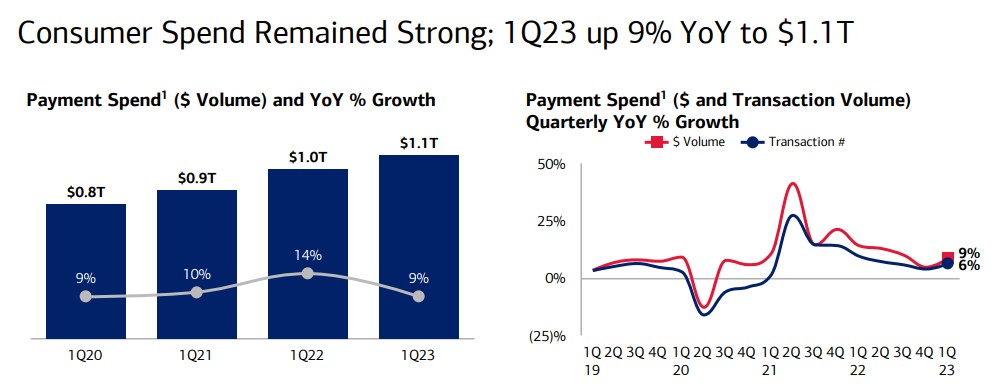

Financial institution of America noticed a bank card loss charge of two.21% within the first quarter, up from 1.7% within the fourth quarter however down from 3.03% in This fall 2019. Client spending is up 9% y/o/y, and most, however not all of it was pushed by larger costs, with transactions up 6% over the identical time.

Given the spending surge when the economic system reopened, given inflation, and given larger rates of interest, you’ll absolutely have anticipated this quantity to go unfavorable at this level. Possibly we get there subsequent quarter, or possibly we don’t, however both approach, the resilience right here is tremendous spectacular.

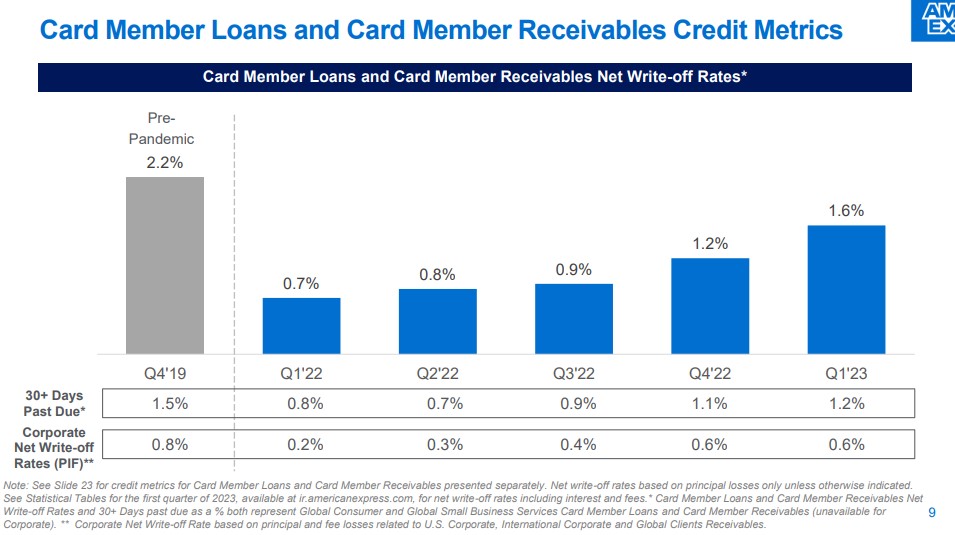

American Categorical additionally confirmed that bank card losses are rising, however nonetheless nicely beneath pre-pandemic ranges.

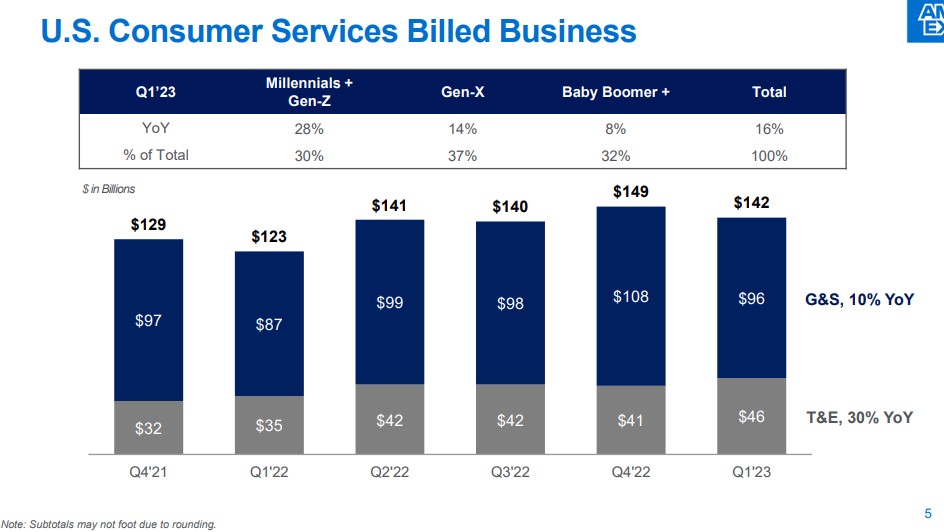

Amex reported a document excessive in income for the quarter, with nearly all of it coming from youthful folks:

“We acquired 3.4 million new playing cards in the course of the quarter…Demand from Millennial and Gen Z customers continues to gasoline this development, accounting for greater than 60 p.c of all new shopper account acquisitions within the quarter. Millennial and Gen Z clients additionally continued to be our fastest-growing U.S. cohort when it comes to spending, rising 28 p.c from a yr earlier.”

If you put all of it collectively, it truly is unbelievable how a lot we’ve been by means of over the previous few years. And the truth that we’ve managed to get this far with out the wheels fully falling off says one thing about our economic system that I don’t suppose needs to be discounted. We’re resilient. We are able to take a punch. We maintain going.

There are many causes to be involved going ahead, however I needed to take a breather from what the longer term would possibly maintain to mirror on what we simply went by means of.

[ad_2]