[ad_1]

Let’s stroll by means of a fast thought train:

What number of householders might afford the month-to-month fee on their home at present ranges of mortgage charges and residential costs?

Take the present worth of your house, subtract 20% for a down fee and slap a 7% mortgage charge on it. May you afford it?

I did this for my home. The month-to-month fee can be almost 3 times what we’re at the moment paying!

To be honest, our 3% mortgage charge isn’t the one motive the month-to-month fee is that a lot decrease. We lived in one other home for 10 years and constructed up fairness that was rolled into our present home.

However my principle is a big share of present householders would have a troublesome time affording the fee on their very own home in the event that they have been compelled to purchase it at prevailing market charges.

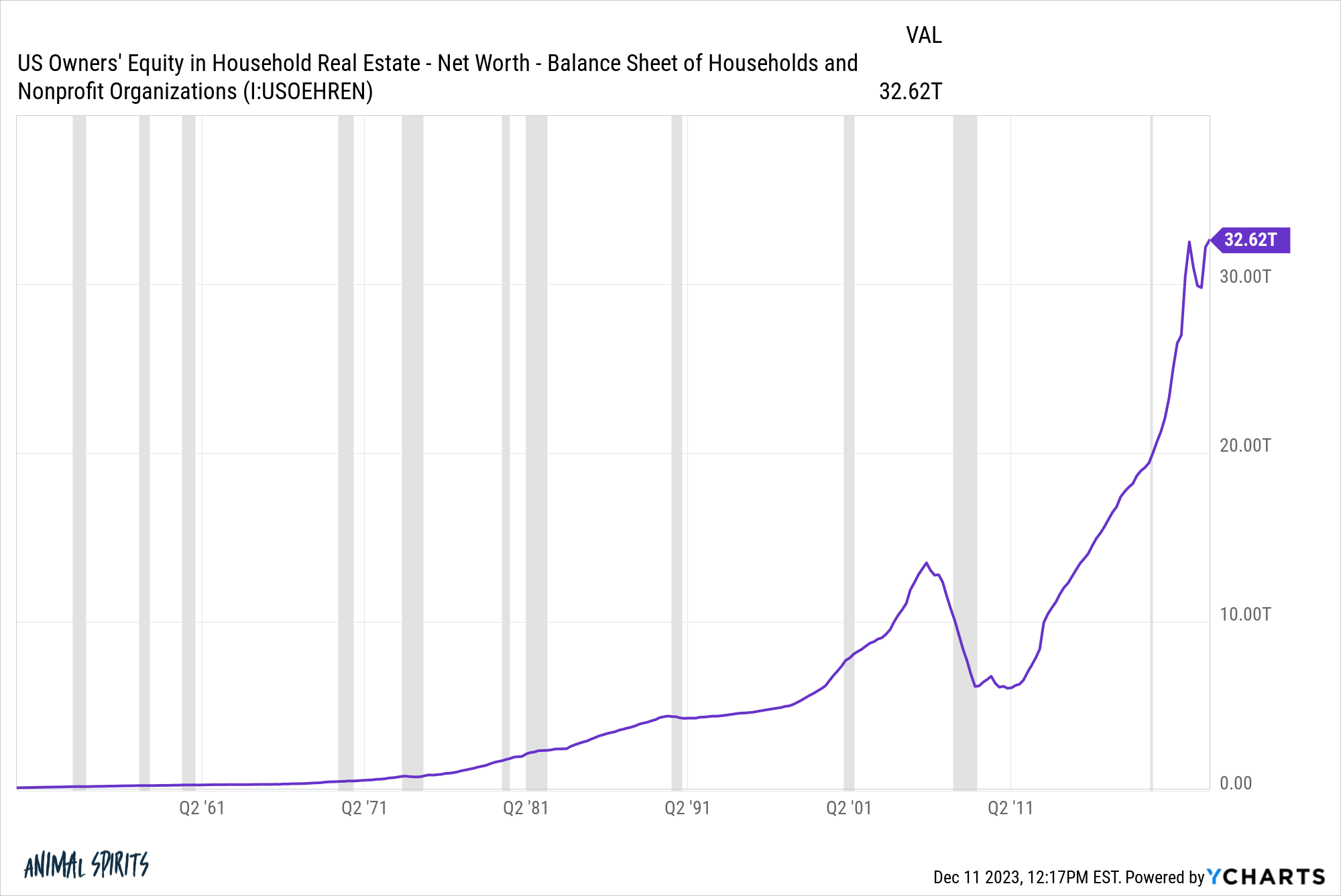

The fairness piece is why this train is solely theoretical. Individuals have an obscene quantity of fairness of their houses proper now:

We’ve gone from $16 trillion in residence fairness on the finish of 2017 to greater than $32 trillion at this time. Dwelling fairness has doubled in rather less than six years.

Housing value good points are a giant motive for the rise however low charges have helped quite a bit too.

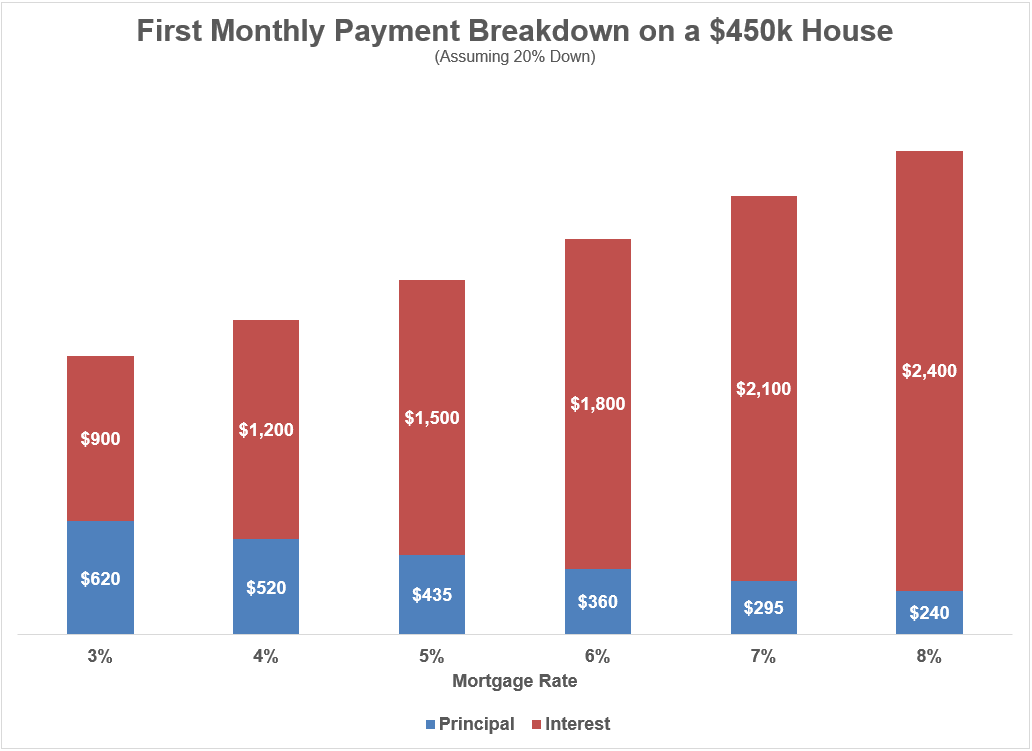

When mortgage charges are 7-8%, a lot extra of your fee goes in the direction of paying curiosity bills.

Right here’s a have a look at the month-to-month fee breakdown by principal and curiosity expense for a $450k home, assuming 20% down at varied 30 12 months mortgage charges:

At decrease mortgage charges, extra of your fee goes in the direction of principal on the outset of the mortgage. Plus homebuyers should purchase larger and higher houses at decrease charges as a result of your fee goes additional.

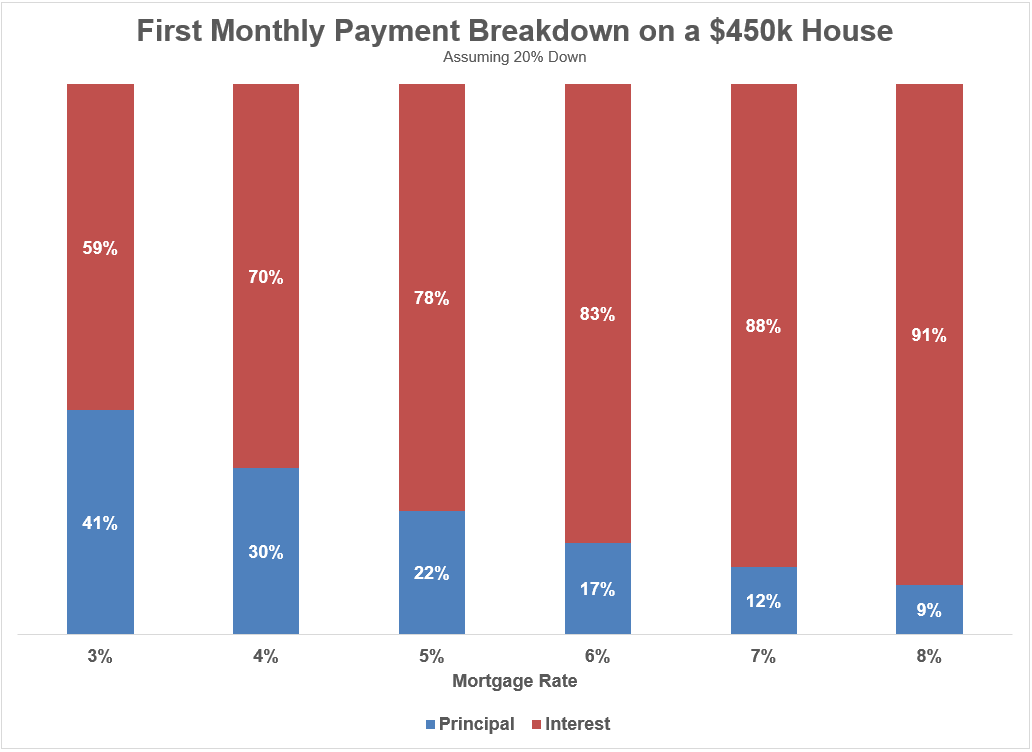

Now have a look at this similar instance on a relative foundation:

Over 90% of your first fee goes in the direction of curiosity expense on an 8% mortgage. Against this, it’s lower than 60% on a 3% mortgage charge.

Over the course of the primary 5 years of the mortgage utilizing these assumptions:

- at a 3% charge, 44% would go to principal paydown whereas 56% of funds would cowl curiosity expense.

- at an 8% charge, simply 11% would go to principal paydown whereas 89% of funds would cowl curiosity expense.

I’m usually not a fan of shopping for a starter residence in hopes of buying and selling up in a couple of years as a result of the prices of shopping for and promoting are excessively excessive. A starter residence trade-in is an excellent worse thought when mortgage charges are increased since you’re barely constructing any fairness except housing costs rise even additional.

If you happen to have been to remain in an 8% mortgage charge for the lifetime of the mortgage, you’d be paying greater than $590k in curiosity prices. With a 3% mortgage, curiosity expense over the lifetime of a 30 12 months mortgage is $186k.

Clearly, the hope for homebuyers within the present charge setting is that they’ll finally have the ability to refinance at decrease charges. That ought to assist.

However the numbers are eye-opening from the angle of a first-time homebuyer.

Some would say it is a return to normalcy within the mortgage charge market.

The typical 30 12 months mortgage charge for the reason that Seventies is shut to eight%:

The late-Seventies/early-Nineteen Eighties timeframe was an outlier however even in the event you have a look at the typical since 2000 it’s been extra like 5%. So the sub-3% pandemic charges have been a historic outlier as properly.

There are at all times going to be winners in losers within the capitalist system beneath which we function.

However these winners and losers are not often determined in a such a brief window in one thing as large and essential because the housing market.

There are many householders who’ve benefitted from the pandemic housing growth.

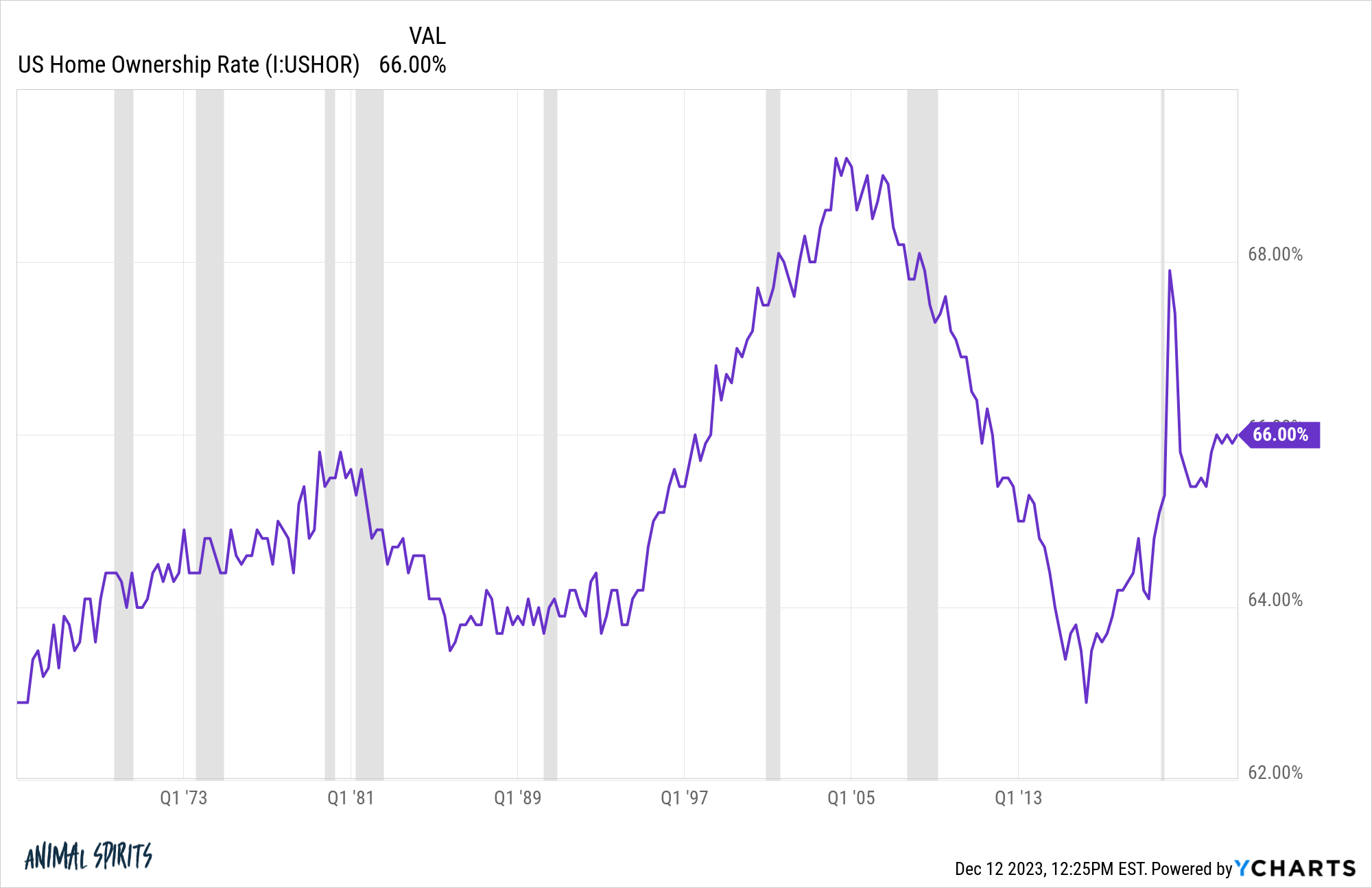

The homeownership charge hasn’t been impacted by at this time’s unhealthy affordability ranges simply but however I’m guessing we’ll see this tick down within the years forward.

The dangerous information for patrons is housing costs and mortgage charges are up.

The excellent news is we’ve skilled one thing comparable on this nation earlier than. Housing costs skyrocketed within the Seventies and Nineteen Eighties following the massive uptick in inflation. Mortgage charges went to double-digit ranges.

It was painful to purchase. However many individuals nonetheless did due to profession or household or an funding or all the different causes folks purchase a home.

They slowly however absolutely constructed fairness. They refinanced. They renovated. The moved.

It won’t really feel prefer it proper now however that can occur once more this time as properly. Housing exercise will thaw out and folks will start transferring once more.

Simply rely your self fortunate in the event you owned a house earlier than costs went skyward and mortgage charges have been traditionally low.

Most owners seemingly couldn’t afford to purchase their very own home proper now in the event that they have been compelled to pay present costs and borrowing charges.

Additional Studying:

Why Are Mortgage Charges So Excessive?

[ad_2]