[ad_1]

The insurance coverage business is experiencing a rising expertise scarcity. Whereas this problem has been anticipated, a lot of the dialogue on options is usually generalized to all the workforce. However not each job will likely be impacted in the identical method. As insurers develop, some features will want extra assist, whereas others will likely be higher primed to make use of cognitive know-how, like AI, RPA and extra. This implies some jobs will likely be changed by know-how, different jobs will likely be enhanced by know-how and different jobs would require extra people (an space the place folks can shift to, if their job is changed).

The very fact is that insurance coverage operations are altering, and individuals are the middle of that change. The query isn’t, “How will we tackle this workforce hole?” The query is, “How will claims, underwriting and gross sales be impacted by this workforce hole, and the way can we leverage know-how to handle each to enhance our operations holistically?” That’s what I’ll be exploring right here.

Urgency wanted to handle the rising workforce hole in insurance coverage

In June 2021, the US Chamber of Commerce launched the The America Works Report with alarming statistics:

- Lower than 25% of the insurance coverage business is beneath 35 years previous.

- Within the final 10 years, insurance coverage professionals aged 55 and older elevated by 74%.

- The Bureau of Labor Statistics estimates that over the following 15 years, 50% of the present insurance coverage workforce will retire.

- There will likely be greater than 400,000 open positions unfilled over the following decade.

These statistics paint a startling image—and one which requires an pressing response. However an ageing workforce isn’t the one concern:

- Insurance coverage corporations are additionally making an attempt to develop, that means they both want a bigger workforce or the power to scale with the present dimension workforce.

- Many instances, there’s a abilities mismatch the place the present insurance coverage workforce lack the abilities wanted to function in an automatic and information centric atmosphere.

- Whereas insurance coverage corporations don’t all the time want lots of of elite tech engineers, they do want their justifiable share of foundational and complimentary technical specialists, particularly because the concentrate on AI/ML and the cloud continues to extend. This will create expertise competitors with huge tech corporations that supply greater salaries, extra perks and extra progressive work.

Tackling the workforce hole holistically

Realistically, the business will be unable to interchange 400,000 open positions one-to-one. And even when it did, the quantity of information loss with 50% of the workforce retiring is big. That is the place cognitive know-how is available in as a part of the answer.

It’s essential to emphasise that know-how is just half of the workforce hole resolution. Whereas extra administrative, redundant duties may be automated, different features may have extra folks (like sales-related areas, which I’ll discover intimately later).

Insurers must do two contradictory issues on the similar time: Have a look at their workforce individually and holistically. Resolution makers must know the influence of the workforce hole and the supporting applied sciences for every particular person job perform. However since jobs don’t function in silos (a minimum of, they shouldn’t), insurers additionally must have a holistic understanding of how adjustments will influence the way in which totally different features work together with and assist one another. In the end, there isn’t a one-size-fits-all resolution. However there are essential insights for all insurers to contemplate.

Cognitive know-how is altering the insurance coverage workforce

Cognitive know-how will influence totally different jobs in numerous methods. Some jobs will likely be changed by automation; others will likely be augmented by know-how; and different jobs might want to develop the human workforce in tandem with know-how.

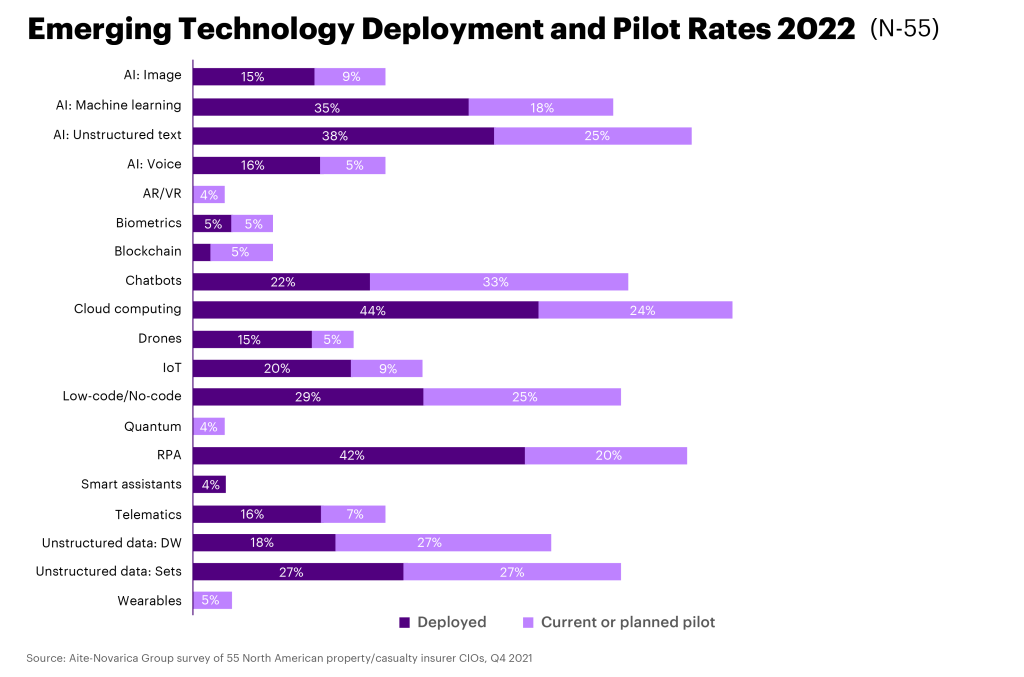

Earlier than leaping into particular job features, it’s essential to know the forms of know-how which might be turning into increasingly more ubiquitous. The next desk highlights the know-how P&C insurers are specializing in in 2022.

Clearly, AI, information and RPA are main areas of focus. Chatbots are additionally getting used extra typically to enhance customer support, whereas cloud and information stay key areas for operational efficiencies and insights. Every of those applied sciences will influence jobs in numerous methods. Let’s discover.

The importance of partnerships

A fast word on the significance of partnerships: You’ll discover all through the examples beneath that nearly each considered one of them is completed by way of a partnership. With tech expertise turning into more durable to seek out, partnerships will likely be a key technique to bridge the expertise hole and implement advanced know-how at scale—and rapidly.

The future of claims: Replace and augment

To handle the workforce hole in claims, know-how will likely be used to each substitute and increase staff, although the size of this influence will likely be totally different between private and industrial strains.

Private:

Private claims is essentially the most susceptible to automation, particularly for easy claims. A small car parking zone automotive accident is an ideal instance of a simple kind of declare that AI can deal with—with human spot-checking, in fact.

Actual-life tech instance: Hippo not too long ago partnered with Claimatic and 5 Sigma to make use of automation to course of householders’ claims quicker and handle them end-to-end. From a buyer perspective, this provides a single level of contact, quicker response instances and simpler claims monitoring. From an operations perspective, this automation reduces back-end friction and ensures accuracy by figuring out the severity of a declare and flagging when a loss is recognized.

Worker influence: There’ll probably be an worker scale-down of the claims workforce as automation manages extra of the claims course of. On the similar time, remaining staff will likely be augmented with know-how to assist them to handle claims quicker and extra precisely. Trying on the Hippo instance, a part of its new automation know-how is to match claimants with adjusters—a sometimes guide, time-consuming course of. This augments the claims workforce in order that they will keep away from a majority of these administrative duties and concentrate on what issues: the shopper.

Business:

Like private strains, industrial claims departments will likely be each changed and augmented by cognitive know-how, however at a special fee. Business claims are sometimes extra advanced, so there will likely be extra augmentation versus substitute, in comparison with private strains.

Actual-life tech instance: Protecting insurance coverage partnered with Roots Automation to scale its trucking and industrial auto insurance coverage claims. In solely 4 months, Protecting launched two “digital co-workers” referred to as Roxy (for sending letters to claimants) and Rex (for indexing claims paperwork). Each bots had been capable of full 95% of duties with out human intervention.

Worker influence: Most claims staff working in industrial strains will likely be augmented by cognitive know-how. The Protecting insurance coverage instance reveals how bots may be leveraged to handle essentially the most time-consuming duties, like indexing paperwork. This frees up staff to concentrate on extra essential duties or deal with extra claims. That is particularly essential for the underserved small-to-medium enterprise (SME) market. By streamlining industrial claims as a lot as doable, the SME market might look extra engaging to insurers.

The way forward for underwriting: Increase

Underwriting encompasses each threat evaluation and product growth. This can proceed to be a key space for insurers to stay trendy and aggressive, so headcount will probably not be reduce. Nonetheless, individuals are retiring. Insurers should ask themselves: Can we substitute retiring employees or use know-how to scale up our present workforce? With the present expertise hole, that latter is extra real looking. This implies underwriting is shifting right into a world of semi-automation, each for private and industrial strains. And which means re/upskilling.

Actual-life tech instance (private): Product growth is a large a part of underwriting, and a whole lot of insurers are leveraging cognitive know-how to make the precise merchandise on the proper time. Arbol partnered with RealTimeRental to supply real-time parametric climate safety for trip leases utilizing AI, analytics and third-party information. AXA Life & Well being Reinsurance Options makes use of a white-labeled model of Verisk’s Well being Danger Ranking Software they’ve branded because the Clever Medical Acceptance Software (IMPACT) to automate elements of the medical insurance underwriting course of to allow higher protection for purchasers with pre-existing circumstances.

Actual-life tech instance (industrial): On the industrial facet, threat is the core theme for cognitive know-how. Allianz SE partnered with Cytora to faucet into AI-based threat processing for its industrial strains enterprise, permitting underwriters to concentrate on value-adding duties. One other instance is insurtech Neptune Flood, which developed an AI-based ranking and quoting platform for automated threat evaluation. With this know-how, Neptune noticed 400% development and is now the most important non-public flood MGU within the US.

Worker influence: Know-how is already altering underwriting, particularly from a product growth and threat evaluation standpoint. Reskilling the workforce will likely be crucial. Know-how, specifically the power to ingest third-party information leveraging the pressure of the cloud, could make product growth quick and nimble. Employees might want to really feel comfy trusting new information sources and AI to drive innovation. Taking a look at threat evaluation, a human perspective will all the time be essential. However underwriters may be knowledgeable and supported by AI and different cognitive know-how to enhance accuracy and make higher choices. Workers will should be reskilled to modernize their strategy and reap the benefits of the large-scale evaluation supplied by AI and different applied sciences.

The way forward for gross sales: Increase and develop

It’s not shocking that gross sales and its related features, like advertising, might want to scale with digital tech. Gross sales should get extra progressive as competitors grows and prospects demand a seamless expertise. New areas, corresponding to embedded insurance coverage, will leverage know-how and technique in a method the business has by no means completed earlier than. To assist this fast shift and development, gross sales features might want to broaden whereas additionally being augmented with know-how.

Actual-life tech instance (private): Direct Auto & Life Insurance coverage selected Advertising and marketing Evolution’s buyer journey monitoring resolution. This persona-based advertising measurement and optimization platform will present insights into the touchpoints prospects have interaction with alongside their path to buy. These insights will assist Direct Auto & Life Insurance coverage to higher perceive its prospects, ship a customized expertise and critically—easy methods to hyperlink conduct to gross sales.

Actual-life tech instance (industrial): Nationwide expanded its relationship with Amazon Net Companies to innovate and deploy progressive merchandise whereas in addition they streamlined inside operations. From a gross sales industrial perspective, this partnership helped Nationwide construct a Small Enterprise Advisory platform that makes use of machine studying to tailor personalised insurance coverage coverage suggestions to small enterprise prospects in minutes.

Worker influence: Gross sales, advertising and buyer engagement are crucial for development. Workers in these areas will likely be augmented with know-how, whereas groups broaden headcount. To stay aggressive, insurers might want to innovate and construct a enterprise growth ecosystem. Know-how by itself gained’t do that. Like underwriting, cognitive know-how will provide the instruments for inventive salespeople to innovate—and the shopper insights to make data-driven choices and promote development.

Roadmap to the longer term: A cross-functional perspective

As I discussed earlier than, job features don’t function in silos. So, this breakdown will get extra sophisticated after we have a look at how every perform interacts with one another. For instance: Claims and underwriting are intertwined. Modernizing claims to higher leverage the information utilized in underwriting and vice versa is extra essential than ever. Breaking down these silos will drive an enterprise stage change in behaviors and collaboration.

That’s why insurance coverage corporations must take a cross-functional perspective when figuring out how know-how will change their workforce. And this shouldn’t be a theoretical technique.

Methods to use tech to shut the insurance coverage workforce hole

Insurers ought to put collectively a concrete workforce roadmap. The roadmap must be modular, outlining which areas will want new hires versus reskilling. It ought to think about the interplay between features and the way altering one will influence the opposite. It must also point out the place folks may be moved round to capitalize in your present workforce and the information and expertise that they’ve.

One other key factor of evolving your workforce is early inclusion. Workers deserve transparency in terms of how their jobs will change. Early involvement will assist staff really feel like they’re part of that change—and decrease substitute fears. As a result of all of the roadmaps on this planet gained’t assist if staff really feel threatened and reject change. Insurance coverage corporations can keep away from this by being supportive, trustworthy and by listening.

Whereas a roadmap and transparency are essential from an worker perspective, the know-how facet is its personal area. This weblog seemed on the product and repair facet of the insurance coverage workforce, however implementing cognitive applied sciences requires a gifted, motivated IT staff. Insurers might want to marry a tech roadmap that aligns with its workforce imaginative and prescient utilizing agile methodologies to permit for flexibility and pivots, if wanted. Critically, executives want to have the ability to talk this holistic imaginative and prescient throughout the group—together with tech companions.

The insurance coverage business has a tricky highway forward in terms of expertise. Many years’ value of information is about to be misplaced to excessive retirements, and youthful generations aren’t banging down the door to work in insurance coverage. Carriers might want to get inventive utilizing a mixture of know-how and a reskilled human workforce to shut this hole and drive future development. The time for this transition is now, or else you threat falling behind. Simply keep in mind that staff are folks—deal with them with respect and compassion, and they’ll rise to your expectations. As we are saying at Accenture: Innovation occurs the place know-how meets human ingenuity. The insurance coverage business will want each to achieve the longer term.

Remodeling claims and underwriting with AI: AI has emerged because the crucial differentiator within the insurance coverage business when utilized in tandem with people.

Get the most recent insurance coverage business insights, information, and analysis delivered straight to your inbox.

Disclaimer: This content material is offered for common info functions and isn’t meant for use instead of session with our skilled advisors.

Disclaimer: This doc refers to marks owned by third events. All such third-party marks are the property of their respective house owners. No sponsorship, endorsement or approval of this content material by the house owners of such marks is meant, expressed or implied.

[ad_2]