[ad_1]

Store native. Eat native. Insure native? Properly, perhaps.

Or, perhaps it’s the philosophy that issues. Perhaps if insurers develop of their understanding of SMB firms, they could simply take that native, distinctive, one-of-a-kind philosophy and apply it in sudden methods that can thrill SMB house owners. In spite of everything, many SMB house owners are drawn to suppliers and clients that know them and their enterprise. Insurers which are serious about increasing throughout the SMB market ought to ask and reply a couple of essential questions.

- What would it not take for insurers to align themselves with firms by discovering the synergies between them, then treating every enterprise as if it’s the solely firm round?

- How can insurers develop giant, act small, and higher fill SMB insurance coverage voids with precision gross sales and impeccable timing?

- Is there a correct method to strategy the insurance coverage relationship that goes past product growth and good service, reaching into the guts and soul of an SMB and the SMB tradition?

- Is as we speak’s SMB enterprise mannequin able to reap the benefits of insurance coverage partnerships and embedded channels?

Answering these questions received’t be simple, however the solutions could kick-start your organization’s concepts on the way it can adapt and develop in these altering instances.

Annually, Majesco demystifies SMB buyer sentiment with a beneficial survey that ends in an especially informative report. As a result of we’ve been asking most of the identical questions, plus including new questions every year (See this yr’s sentiment concerning the Metaverse. You can be astounded!), now we have the power to understand quick and long-term SMB traits. We then relate these traits and name out the highlights. It’s the background for answering our questions above.

This yr’s SMB shopper report, Resiliency in Instances of Change: Rethinking Insurance coverage to Assist SMBs Thrive, accommodates a bunch of insights on how insurers can place themselves, not simply as educated, however as sought-after companions within the enterprise. In as we speak’s weblog, we give a high-level overview of why these insights matter for insurers.

From an insurance coverage perspective, a enterprise is not only a enterprise.

A November 2022 NFIB report encapsulates the state of the small-medium enterprise market and the challenges they’re going through. There are actually pressures upon small companies, however all shouldn’t be bleak. In a ballot performed by Guidant Monetary, 65% of small enterprise house owners reported being worthwhile, with 51.04% seeking to improve employees. Much more promising, 41% wish to increase or transform their enterprise, and 39% plan to spend money on digital advertising.[i]

This presents a possibility for insurers to supply the fitting merchandise, value-added providers, and experiences to assist SMBs navigate these challenges and place their companies for progress in a world of accelerating local weather, societal and expertise dangers.

Every enterprise is its personal little insurance coverage nut to crack. Each enterprise wants insurance coverage, however in addition they want a lot extra. Similar to insurers are rising extra comfy with experimentation, SMBs thrive on experimentation and adaptability — the very issues which will open alternatives for threat protection.

“As a result of they’re not slowed down by paperwork,” says SMB knowledgeable, Peter Boumgarden, Director and Professor of Observe, Washington College, “small companies are sometimes in a position to experiment and pursue new alternatives extra simply. If I had been a small enterprise proprietor, I might be asking what sorts of small experiments I can run within the subsequent six months that assist me handle the approaching headwinds.”[ii]

It’s extra necessary than ever for insurers to have strategic discussions on how they are going to plan, prioritize, finances, and handle the adjustments wanted of their enterprise fashions, merchandise, channels, and expertise. The extra SMBs are keen to experiment, the extra methods insurance coverage could discover to become involved with services or products in assist.

Resiliency in Instances of Change

Small-medium enterprise is the lifeblood and spine for many markets. The SBA notes there are 32.5 million companies within the US, representing 99.9% of all companies. Likewise, SMBs have been essential to the COVID financial restoration. And SMBs are now not run by the older technology. Millennials and Gen Z are 188% extra probably than Boomers to point they are going to probably create a aspect enterprise![iii]

Collectively, these information factors mirror SMBs’ resiliency – from financial to generational adjustments – by investing and adapting via accelerated digitalization, shifting to on-line channels, rethinking the enterprise mannequin, and providing new merchandise. Their outstanding resilience and capability to adapt and innovate their companies have allowed them to outlive and thrive as we speak and sooner or later.

Similar Challenges however Divergent Views

Our survey reached two equally sized generational SMB segments, Gen Z and Millennials and Gen X and Boomers, to evaluate their enterprise priorities, expectations, and insurance coverage wants and the way their distinctive traits affect them.

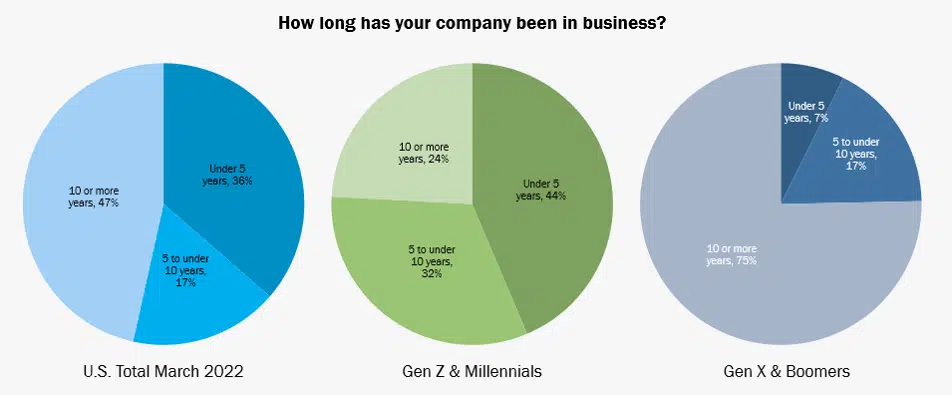

Gen Z and Millennial enterprise leaders have youthful companies, with 44% of their companies being lower than 5 years outdated — in comparison with 7% for Gen X and Boomers as mirrored in Determine 1. Gen Z and Millennial companies underneath 5 years outdated are in keeping with the entire U.S. statistic for this group of 36%. What’s most attention-grabbing is that the youthful technology has 76% with a enterprise 10 years or much less and the older technology has 75% ten years or extra – a whole distinction between the 2 generational teams.

This distinction is necessary for insurers when it comes to the merchandise and buyer experiences they ship. The youthful technology has began and grown their enterprise absolutely within the throws of the digital age whereas the older technology didn’t. Their wants and expectations in consequence are vastly totally different when it comes to their operations, using expertise, and far more.

Determine 1: Distributions of enterprise ages, whole U.S. and by generations

After we additional have a look at the industries they comprise and evaluate between the 2 technology segments, a couple of key variations emerge. These variations additional mirror their age and expertise distinctions which affect their enterprise priorities, expectations, and insurance coverage wants.

The highest three industries for Gen Z and Millennials respondents are Building/Residence Enchancment, Computer systems ({Hardware}, Software program), and Retail. For Gen X and Boomers, it’s Building/Residence Enchancment, Enterprise/Skilled Companies, and Different. A key distinction between the 2 segments is Pc ({Hardware} and Software program) and Retail, reflecting the digital variations between the generations. And the necessity for various merchandise given their companies are probably extremely digital.

Prime-of-Thoughts Points

The survey outcomes mirror the difficult and unsure instances SMBs are going through, together with inflation, provide chain challenges, rising rates of interest, and low unemployment. Those that survived the financial fallout of COVID did so by pivoting and adapting their enterprise fashions to function digitally, increase channels and merchandise, and rethink staffing necessities.

As new financial challenges proceed or intensify, the precedence for adapting, innovating, and accelerating digital transformation with expertise will increase. These priorities affect enterprise threat and insurance coverage wants for SMBs.

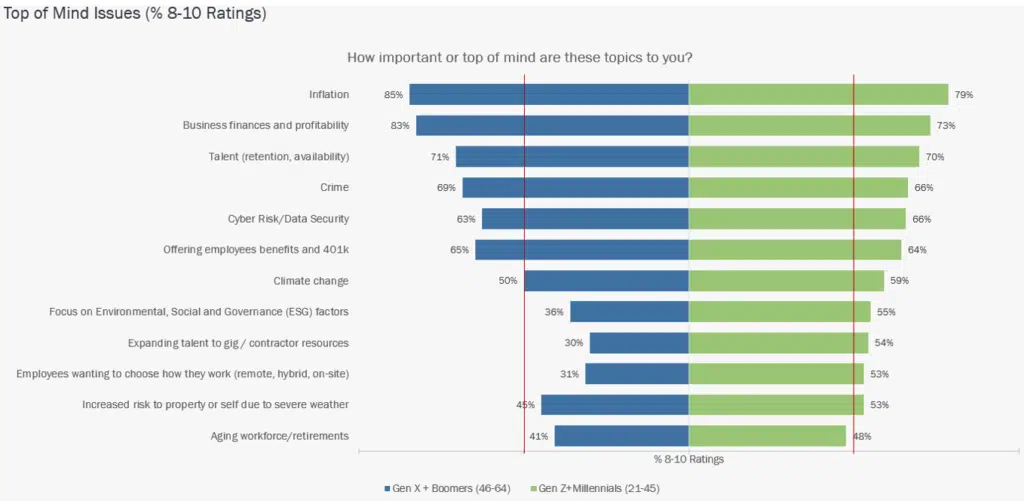

On the prime of the listing is inflation, at 79% for Gen Z and Millennials and 85% for Gen X and Boomers as proven in Determine 4. Millennials and Gen Z are wrestling with sharp value will increase for the primary time since they’ve been sufficiently old to note, as reported by the New York Instances.[iv]

Associated to that is the affect of inflation on enterprise funds and profitability at 73% and 83%. Consequently, SMBs will probably be taking a look at operational price financial savings and the confirmed worth of services, together with insurance coverage. Insurers should give attention to merchandise that adapt to their wants, guarantee pricing is perceived as honest, clear, and correct, and supply value-added providers that assist them of their every day operations or cut back threat and price to their enterprise.

Determine 2: SMBs’ prime of thoughts points

Additional difficult SMBs at quantity three is expertise retention and availability (70%, 71%). The Nice Resignation continues to irritate expertise recruitment and retention, pushing worker advantages and 401k plans to a powerful top-of-mind concern (64%, 65%), at quantity six.

The altering threat panorama, significantly for societal and expertise threat is mirrored within the quantity 4 concern of Crime (66%, 69%) and the quantity 5 concern of Cyber/Knowledge Safety (66%, 63%). With the price of insurance coverage rising and a significant expense merchandise for many companies, the rise in crime charges and cyber incidents and the associated improve in insurance coverage prices have change into a key concern for SMBs. Insurers who present value-added providers round threat administration to assist SMBs spend money on loss prevention, proactive HR practices and aggressive claims administration will probably be seen extraordinarily favorably. It’ll differentiate them out there.

Apparently the most important gaps between the generational segments are views on ESG elements (19% hole), use of Gig/contractor staff (24%), and workers wanting to decide on how they work (22%). In response, some insurers are growing threat appetites primarily based on net-zero and carbon discount pathways, the introduction of sustainable insurance coverage merchandise, and investments into funds that again or assist insurance coverage merchandise.[v]

The important thing perception to those priorities is that there will probably be a better give attention to the varieties of insurance coverage merchandise and the way they’re priced to make sure they align to their broad threat and monetary wants. That is the place their use of digital expertise and different traits are influencing their insurance coverage expectations.

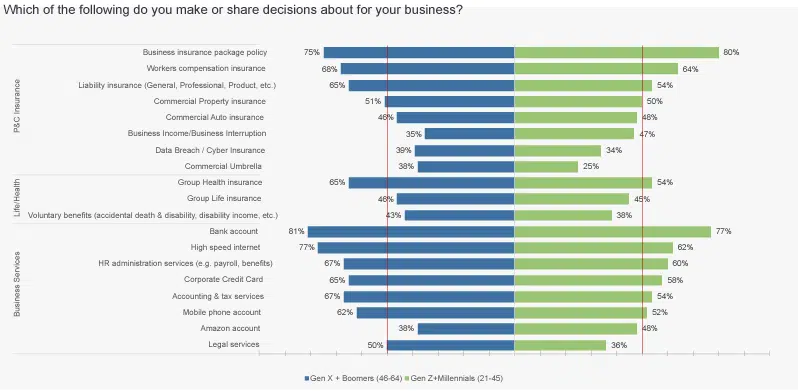

Apparently, each generational teams’ utilization patterns for insurance coverage, monetary, and enterprise services are practically mirror photographs of one another, with a couple of exceptions as mirrored in Determine 5.

Within the P&C Insurance coverage class, the foundational product, Enterprise Insurance coverage, has robust utilization by each generations (80%, 75%) with Employees Comp following (64%, 68%) as the highest two. Gen Z and Millennials have decrease utilization of legal responsibility insurance coverage by 11% (54% vs 65%) and business umbrella by 13% (25% vs 38%) however lead Gen X and Boomers in enterprise revenue/enterprise interruption insurance coverage by 12% (47% vs 35%). Given the affect of COVID, local weather, and societal dangers the dearth of enterprise revenue/interruption insurance coverage could be very low and provides a market progress alternative for insurers.

With the acceleration of digitalization of SMB enterprise fashions famous beforehand, it’s regarding that just about two-thirds of SMBs shouldn’t have information breach/cyber insurance coverage, significantly given cyber threat/information safety is a top-five top-of-mind concern. This highlights the market alternative for insurers to teach and supply cyber insurance coverage to SMBs.

For the Life/Well being class, Gen Z and Millennial SMBs lag behind their older counterparts by 11% in providing group medical insurance (54% vs 65%), and by 5% in voluntary advantages (38% vs 43%). Surprisingly, lower than half of each SMB segments supply voluntary advantages or group life insurance coverage. Provided that expertise availability and retention is their third most top-of-mind concern, this ought to be the next precedence and represents a possibility for insurers to develop enterprise in these strains.

Determine 3: Insurance coverage, monetary and enterprise services utilized by SMBs

Digital Know-how and Enabled Enterprise Merchandise & Companies

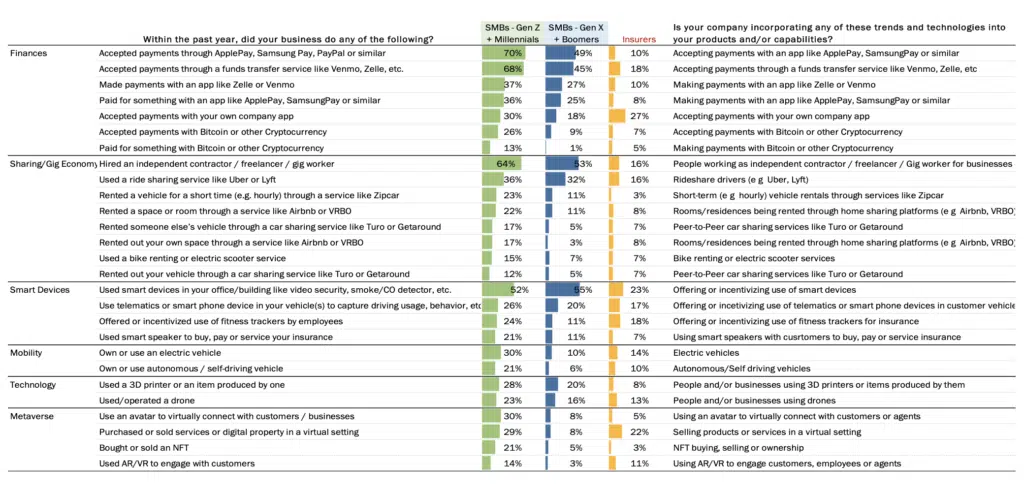

With as we speak’s heightened buyer calls for in addition to thrilling new services and non-insurance choices, new billing and fee strategies are important. Billing and fee options should be constructed to adapt and flex because the market, product, providers, and buyer expectations proceed to shift. Insurers want the pliability to take care of something new that could be thrown at them.

This demand could be very clear with Gen Z and Millennials accelerated acceptance of digital funds via digital wallets like Apple Pay, Samsung Pay, or PayPal (70% vs 64%) and thru fund switch providers like Venmo or Zelle (68% vs 56%) (Determine 6) as in comparison with final yr. In addition they prolonged their lead over Gen X and Boomers in using these digital funds, now at 21% and 22% in comparison with gaps of simply 7% in final yr’s survey.

Moreover, use of sensible gadgets is on the rise for each generational teams, the Millennials and Gen Z at the next stage. Whether or not in autos, on properties or wearables the elevated use of those gadgets supply insurers large alternative for modern new merchandise and value-added providers, in addition to customized underwriting primarily based on their particular threat. The issue is that insurers (a preview of our Strategic Priorities analysis) aren’t maintaining with these expectations.

Determine 4: Use of applied sciences and participation in traits, 2021-2022

Insurance coverage on the Edge

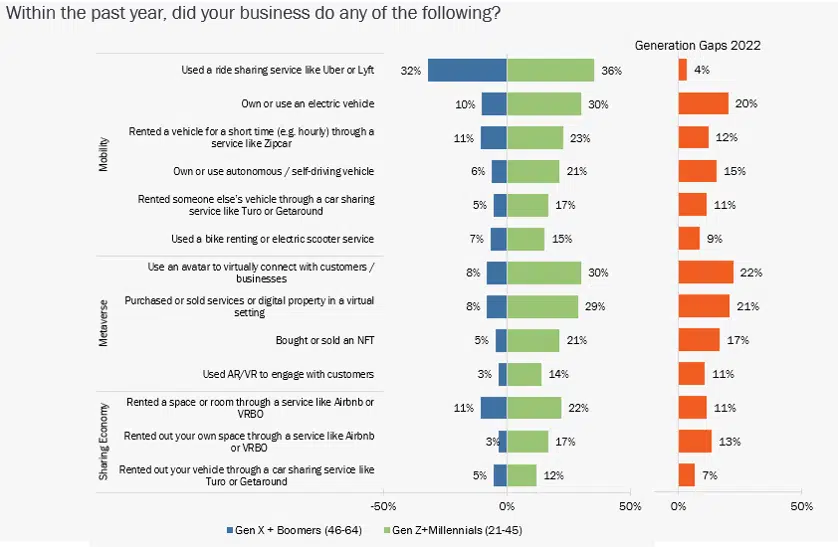

This yr we added three extra classes of business-related actions and applied sciences as seen in Determine 7: Sharing Economic system, Metaverse, and Mobility. Gen Z and Millennials have double-digit leads over Gen X and Boomers in 10 of the 13 particular areas. Standing out are gaps of 20% or better in proudly owning/utilizing an electrical car and, curiously, two Metaverse-related actions, utilizing an avatar to nearly join with clients/companies and buying or promoting digital property in a digital setting.

Inside Mobility, Gen Z and Millennials far outpace the older technology is utilization throughout the board. Particularly, choices past proudly owning and utilizing their very own car play a rising position of their utilization – significantly rental of a short-term car like Zipcar, bike, electrical scooter, or renting another person’s car. There’s continued robust utilization of Uber or Lyft – which for some companies has change into a staple for supply.

Metaverse erupted out there within the final yr with a number of fanfare, but not a number of exercise relative to insurance coverage. Nevertheless, in accordance with PwC, the pervasiveness of the metaverse and the corresponding improve in social and financial actions performed by way of avatars will create new buyer wants and require insurance coverage firms to take a special strategy to serve their clients. The metaverse will speed up the digitization of administrative procedures from contracting to asset administration within the type of NFTs. Crypto belongings could change into extra widespread too.[vi]

Almost a 3rd of Millennials and Gen Z are serious about utilizing an avatar to attach with clients/companies, buying or promoting in a digital setting, and shopping for or promoting an NFT. This highlights the necessity for potential new insurance coverage merchandise and the growing demand for cyber merchandise that particularly handle the utilization of metaverse belongings for youthful SMB house owners.

Determine 5: Use of applied sciences and participation in traits, 2022

Strategizing for Synergy

In gentle of those traits, the main focus for insurers must be, not simply on capturing this yr’s crop of recent companies, however on making a basis for future progress into new areas of merchandise and value-added providers throughout the SMB house, significantly the youthful technology who’ve diverging wants and expectations from the older technology. It’s a market ripe for progress as a result of there’s a rising want indicated by SMBs, however we have to rethink our strategy to the market.

If this overview has your curiosity piqued, get a more in-depth and extra informative look by studying Majeso’s full thought-leadership report, Resiliency in Instances of Change: Rethinking Insurance coverage to Assist SMBs Thrive. It offers you and your groups meals for thought on how, when, and the place you possibly can create product, service, and cultural synergies with the tens of millions of SMBs that want insurance coverage — each throughout the nation and in your personal neighborhood.

[i] “2022 Small Enterprise Tendencies,” Guidant Monetary, https://www.guidantfinancial.com/small-business-trends/

[ii] Savat, Sara, WashU Professional: Constructing small enterprise agility for 2023 volatility, The Supply, January 13, 2023

[iii] Mohsin, Maryam, “10 Small Enterprise Statistics You Have to Know for 2023,” Oberlo, January 1, 2022, https://www.oberlo.com/weblog/small-business-statistics

[iv] Smialek, Jeanna, et al., “Millennials Confront Excessive Inflation for the First Time,” New York Instances, November 28. 2021, https://www.nytimes.com/interactive/2021/11/28/enterprise/economic system/high-inflation-millennials.html

[v] Tripathy, Prashant, “Integrating ESG into insurance coverage merchandise,” Monetary Categorical, July 6, 2022, https://www.financialexpress.com/cash/insurance coverage/integrating-esg-into-insurance-products/2584104/

[vi] “The affect of the metaverse on the insurance coverage {industry},” PwC, July 15, 2022, https://www.pwc.com/jp/en/information/column/metaverse-impact-on-the-insurance-industry.html

[ad_2]