[ad_1]

In line with the Nationwide Affiliation of Realtors, the median value of a home in america is price $190,000 greater than it was a decade in the past.

If you happen to’ve owned a home for greater than 3 years or so, you’re doubtless sitting on some good features.

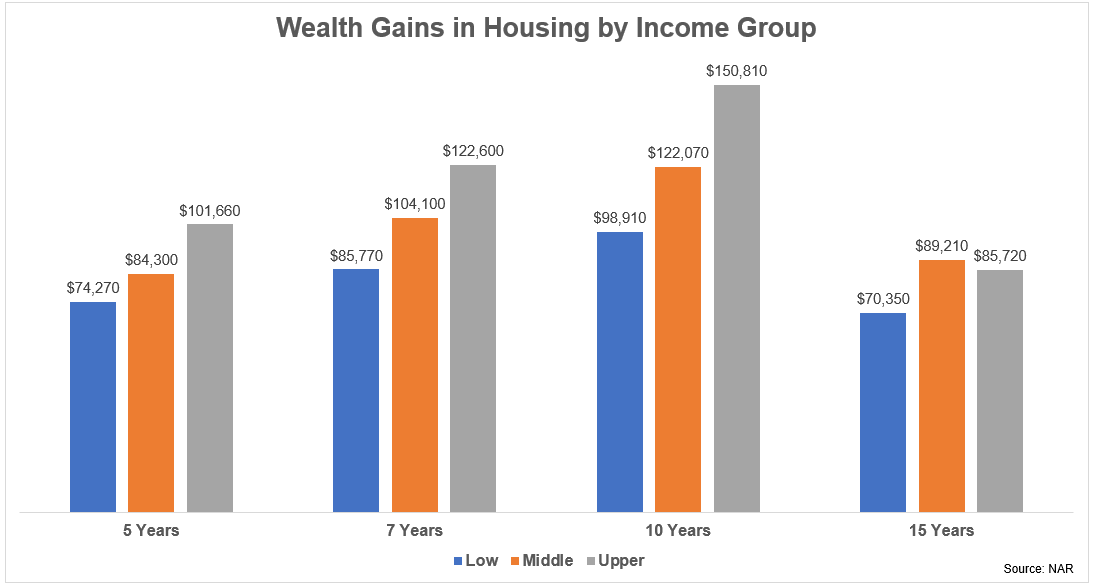

These features weren’t evenly distributed however throughout the varied earnings ranges, owners have made a great chunk of change:

The pandemic-related housing features are not like something we’ve ever seen earlier than so it’s not like you must count on this to proceed.

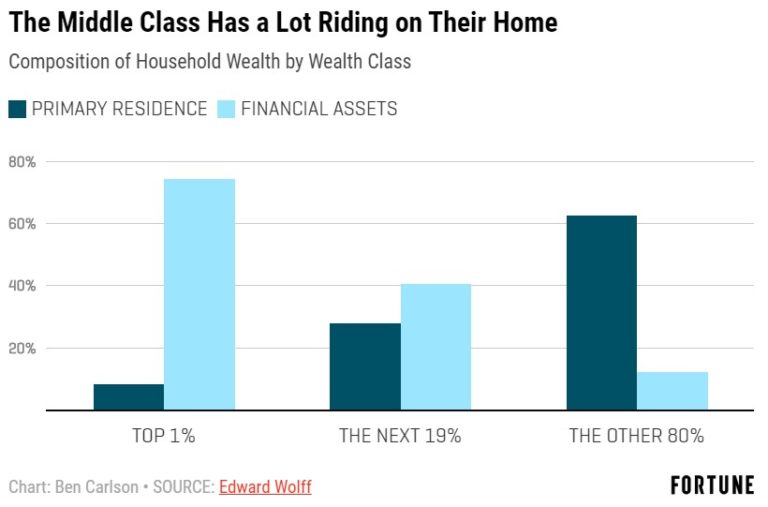

However the housing market is extra vital for the center class than the inventory market for the straightforward incontrovertible fact that possession of residential actual property is extra widespread.

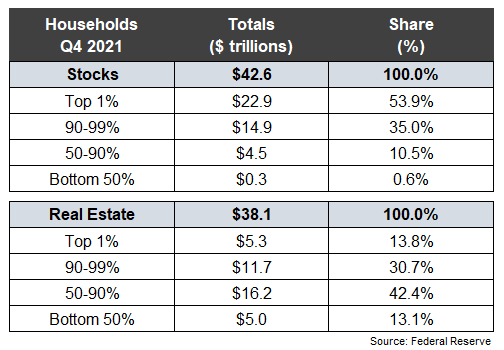

The highest 10% controls almost 90% of the inventory market whereas the underside 90% owns greater than 55% of the housing market:

It’s no enjoyable for individuals who have missed out on the features we’ve seen throughout this cycle however this can be a good factor for individuals who don’t maintain as many conventional monetary belongings like shares and bonds:

There’s, nevertheless, an issue with having your wealth so concentrated in your house.

For one factor, the wealth features cited within the analysis by the NAR are on a gross foundation.

You must web out the entire ancillary prices concerned with homeownership to get the actual quantity. Issues like realtor charges, closing prices, property taxes, shifting bills, insurance coverage, maintenance and upkeep can take an enormous chunk out of any nominal value will increase.

Plus, having your wealth tied up in your own home is far totally different than proudly owning monetary belongings or having that cash within the financial institution.

A house is an illiquid asset. It’s tough to faucet your fairness. There are a lot of choices however none of them are a slam dunk:

- You may open up a house fairness line of credit score or do a cashout refinance however that requires borrowing more cash.

- You may use your fairness as a down cost for a brand new house however that additionally means paying the now increased housing costs.

- You may promote your own home to both downsize or turn out to be a renter however you’re all the time going to need to reside someplace.

- You may carry out a reverse mortgage once you retire however that’s a sophisticated course of.

- You may reside some other place and hire out your private home to supply some earnings however there are nonetheless a number of prices and potential complications concerned in that course of (and once more you must reside someplace).

I’m not attempting to speak individuals out of proudly owning a house. There are many advantages to being a home-owner.

It’s a type of compelled financial savings. It’s a great hedge in opposition to inflation. It lets you lock in a set month-to-month price and develop into your cost over time. And there’s the psychic earnings element that comes from making it your personal and residing in your required group.

Clearly, rising housing costs are higher than the choice in the event you personal your own home. The features we’ve seen have helped households within the center and decrease class construct wealth in an enormous manner over the previous decade or so.

However unlocking the worth in your house shouldn’t be as simple as one may suppose.

Constructing wealth in your house is good however it’s vital to diversify into different monetary belongings as properly.

Additional Studying:

Why the Housing Market is Extra Vital Than the Inventory Market

[ad_2]