[ad_1]

By Max Dorfman, Analysis Author, Triple-I

2023 was one other yr with high-risk local weather and weather-related challenges, with 2024 positioned to pose its personal challenges.

Certainly, 2023 was the warmest yr for the globe since 1850 — when these information have been first made. The temperature in 2023 was over two levels Celsius above the 20th Century common, with the ten warmest years in recorded historical past occurring from 2014-2023. Document-setting temperatures hit areas throughout Canada, the southern United States, Central America, South America, Africa, Europe, Asia, in addition to elements of the Atlantic Ocean, the Indian Ocean, and South Pacific Ocean.

These shifts in world climate – mixed with altering inhabitants and different dynamics – have performed a strong position within the danger of disasters.

Prices are excessive

In the US, Allianz estimates, excessive climate occasions now price the nation $150 billion a yr, making these perils “key threats” for organizations. Nonetheless, bigger firms are main a response to those dangers by remodeling their enterprise fashions to low carbon, whereas additionally creating new and improved plans to answer local weather occasions. Allianz notes that supply-chain resilience is a vital space of focus for the approaching yr.

“Though this yr’s Allianz Threat Barometer outcomes on local weather change present that reputational, reporting, and authorized dangers are considered lesser threats by companies,” stated Denise De Bilio, ESG Director, Threat Consulting, Allianz Industrial, “many of those challenges are interlinked.”

Based on Allianz, publicity stays highest for utility, vitality, and industrial sectors. Final yr’s wildfires in Canada restricted oil and fuel output to three.7 p.c of nationwide manufacturing. Water shortage is now additionally thought-about to be a risk.

Promising developments

As Triple-I reported in late 2023, regardless of all the priority relating to local weather danger, sure weather-related disasters truly declined previously yr. This contains U.S. wildfire, which noticed its lowest frequency and severity previously 20 years, regardless of catastrophic losses in Washington State, Hawaii, Louisiana, and elsewhere, in keeping with a Triple-I Points Transient. California – a state typically thought-about synonymous with wildfire – final yr skilled its third gentle hearth season in a row.

Owners insurance coverage charges in California, as elsewhere in the US, have been rising. A few of this development is because of wildfires and development within the wildland-urban interface, which put elevated quantities of costly property in danger. Based on Cal Hearth, 5 of the most important wildfires within the state’s historical past have occurred since 2017.

A lot of California’s drawback, nonetheless, is expounded to a 1988 measure – Proposition 103 – that severely constrains insurers’ potential to profitably insure property within the state. Late in 2023, California Insurance coverage Commissioner Ricardo Lara introduced a package deal of government actions aimed toward addressing among the challenges included in Proposition 103.

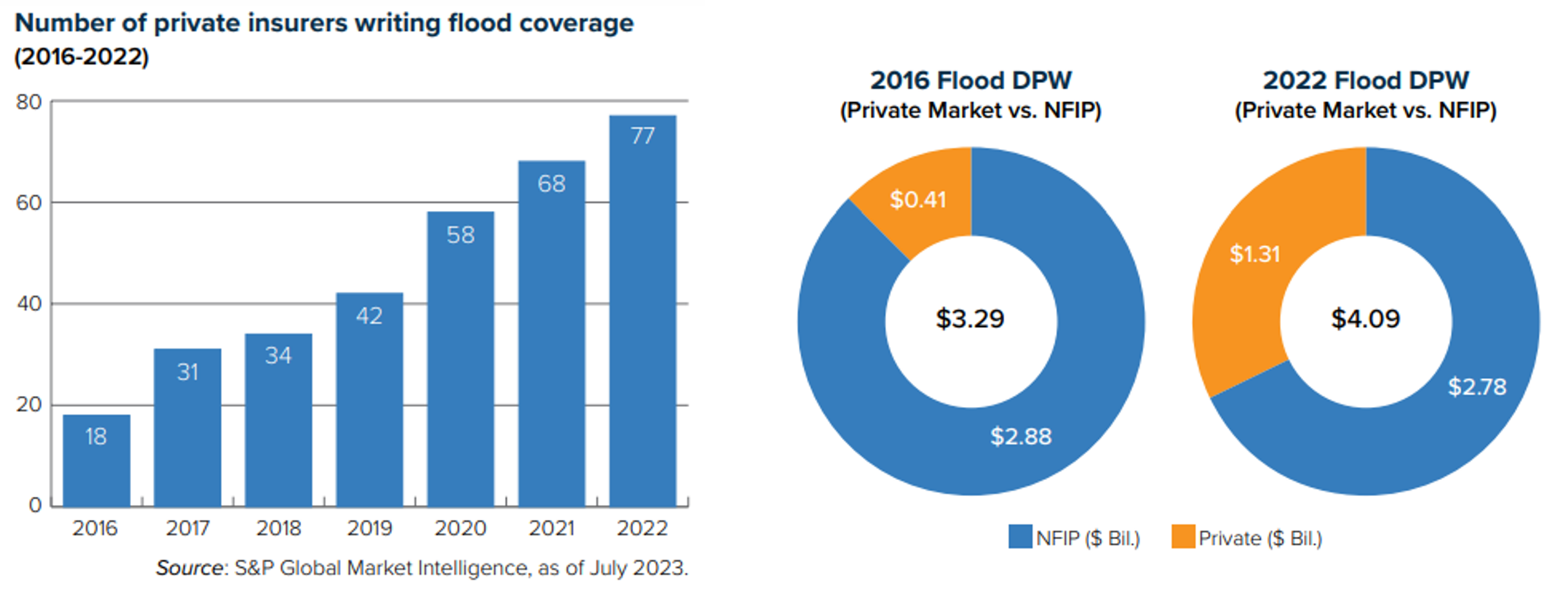

Flood stays a extreme and growing peril in the US. Whereas the federal authorities stays the primary supply of insurance coverage protection by FEMA’s Nationwide Flood Insurance coverage Program (NFIP), the personal insurance coverage market is more and more stepping as much as assume extra of the danger. As Triple-I has reported, between 2016 and 2022, the entire flood market grew 24 p.c – from $3.29 billion in direct premiums written to $4.09 billion – with 77 personal firms writing 32.1 p.c of the enterprise. Because the charts beneath clarify, personal insurers are accounting for an even bigger piece of a rising pie.

This is a vital improvement, because the rising private-sector involvement in flood can moderately be anticipated to end result, over time, in better availability and affordability of flood insurance coverage because the peril will increase and NFIP – by elevated reliance on risk-based pricing – spreads the price of protection extra pretty amongst property house owners. Traditionally, the system typically sponsored protection for higher-risk houses, to the detriment of lower-risk property house owners. With NFIP premium charges rising to extra precisely mirror the danger assumed, personal insurers – armed with more and more subtle information and analytical instruments – are higher outfitted than ever to establish alternatives to write down extra enterprise.

A lot but to be finished

Rising consciousness and motion to deal with climate-related danger is promising, however the disaster is way from over. In a number of U.S. states, insurance coverage affordability and even availability are being affected, and far of the dialog round this subject confuses trigger with impact. Rising insurance coverage charges and constrained underwriting capability is a end result of the danger setting – not a reason for it.

Funding in mitigation and resilience is important, and this can require collective accountability from the person and neighborhood ranges up by all ranges of presidency. It would require public-private partnerships and applicable alignment of funding incentives for all co-beneficiaries.

Be taught Extra:

Triple-I Points Transient: Flood

Triple-I Points Transient: Wildfire

FEMA Reauthorization Session Highlights Significance of Threat Switch and Discount

Miami-Dade, Fla., Sees Flood Insurance coverage Charge Cuts, Because of Resilience Funding

Milwaukee District Eyes Increasing Nature-Based mostly Flood-Mitigation Plan

Attacking the Threat Disaster: Roadmap to Funding in Flood Resilience

It’s Not an “Insurance coverage Disaster” — It’s a Threat Disaster

[ad_2]