[ad_1]

It might shock you to listen to that I, a monetary planner, am not large on making New Yr’s resolutions. Prior to now I’ve resolved to maintain a home plant alive, and perhaps this 12 months I’ll attempt to feed my chunky lab much less human meals (it’s laborious to say no to the Director of Mischief). These small optimizations really feel good, assist us enhance ourselves and others, and encourage us to attempt new issues – I really like that many individuals embrace this! Nonetheless, I choose to concentrate on the massive image of what I would like life to seem like each now and sooner or later, and fewer on “what do I need to do that month or 12 months”. This retains me trustworthy and disciplined concerning the constant actions required to maneuver the needle.

Efficiently assembly long-term objectives requires greater than December thirty first ambition. Whether or not you’re accumulating wealth for objectives like retirement or making a legacy, having fun with the life-style that your wealth permits, otherwise you simply need to be financially unbreakable, constant conduct is a key to success. Learn on for some issues to think about as the brand new 12 months unfolds – current laws might change your strategy to saving and investing for the long run.

Save & Make investments No Matter the Surroundings

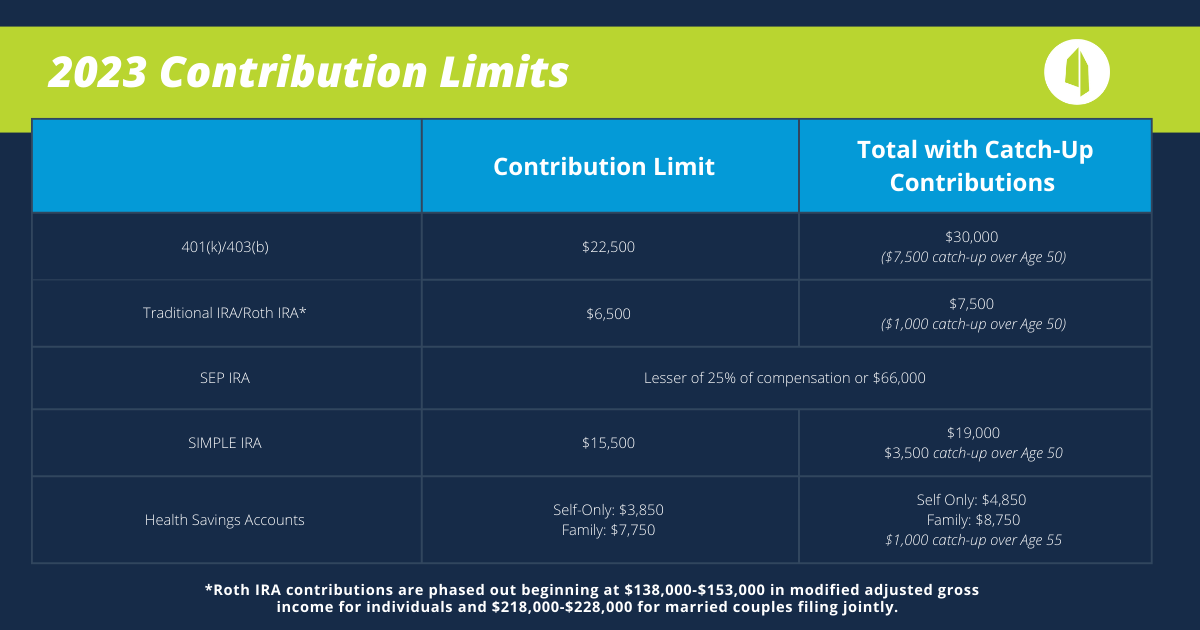

The beginning of the 12 months is a good time to overview present contribution limits for tax-deferred accounts like retirement accounts and Well being Financial savings Accounts. Be sure to are set to effortlessly maximize these as you’re able. Saving and investing persistently whatever the noise on this planet round us is simpler stated than carried out – I’m even responsible of accumulating more money than I would like for wholesome emergency financial savings. Organising common automated contributions to retirement and even taxable funding accounts makes it extra possible that we’ll proceed investing and never get derailed when issues get powerful available in the market like they did in 2022. Our behaviors are a key driver of success when the world round us is unpredictable and outdoors of our management.

Automating doesn’t imply set it and neglect it…limits change yearly (brutal inflation in 2022 had a silver lining in driving larger contribution limits for 2023), and the “Safe Act 2.0” handed in December 2022 as a part of a broader omnibus spending invoice makes issues just a little extra sophisticated.

2023 Contribution Limits

What Modifications with the “Safe Act 2.0”?

Provisions within the “Safe Act 2.0” are set to kick in over quite a few years and can impression how we save for retirement. Not a complete lot is altering in 2023, however there are some things to concentrate on within the near-term as you concentrate on your saving technique. This isn’t an exhaustive checklist however incorporates the small print more than likely to impression you with regards to each saving for the long-term and sustaining tax-efficiency.

A Deal with Roth Cash for Excessive Revenue Earners & Enterprise House owners in Office Plans

· One large change for self-employed people and small companies in 2023 is the introduction of Roth SEP & SIMPLE IRAs. Whereas Roth contributions received’t lower your taxable revenue now, they provides you with flexibility with regards to tax planning sooner or later with the advantage of tax-free withdrawals in retirement.

· Starting in 2024, staff may begin receiving Roth matching contributions from their employer – these contributions can be included within the worker’s taxable revenue. Beforehand, employers may solely make matching contributions on a pre-tax foundation. Not all employer plans have a Roth possibility – however this may increasingly compel extra companies to incorporate a Roth of their plan design.

· Additionally starting in 2024, these over 50 wishing to make catch-up contributions whose wages exceeded $145,000 within the earlier 12 months can be required to make them to a Roth supply of their employer-sponsored plan. Whereas this removes one tax-reduction technique within the type of pre-tax contributions, catch-up contributions to a Roth supply are nonetheless price it with regards to constructing wealth with tax-deferred (and ultimately tax-free) earnings. There are plenty of nuances to this rule – finest to speak via this one with us to see how this would possibly apply to your distinctive scenario!

Greater Catch-Up Limits to Maximize Financial savings

· Beginning in 2024, catch-up contributions for IRAs and Roth IRAs will improve with inflation in $100 increments relatively than remaining a flat $1,000/12 months.

· By 2025, catch-up contributions to office retirement accounts will improve much more for these between 60-63, permitting you to save lots of extra in what could also be your highest-earning years. The improved catch-up would be the larger of $10,000 or 150% of the catch-up contribution quantity from the earlier 12 months. Remember that the Roth catch up guidelines will apply to these with wages above a specific amount (possible $145,000 adjusted for inflation).

Capacity to Hold Tax-Deferred Funds Invested Longer & Enhanced Tax-Planning Alternatives in Retirement

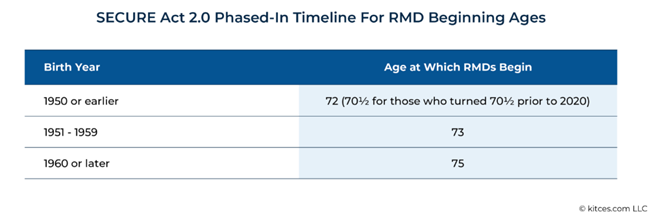

· Beginning this 12 months (2023), Required Minimal Distributions (RMDs) can be obligatory beginning at Age 73, one 12 months later than below the unique “Safe Act”. This can get pushed out even additional to Age 75 by 2032. As a result of nothing is ever completely clear with laws that will get jammed via the week of a vacation, inconsistent language associated to this provision is creating some confusion. This helpful chart from our pals at Kitces.com removes the guess work with regards to realizing when it’s essential to take an RMD:

· By 2024, RMDs from employer-sponsored Roth retirement plans will not be obligatory, making these Roth plans extra like Roth IRAs, the place RMDs aren’t required. This can will let you maintain your Roth {dollars} invested longer in case you nonetheless have cash in an employer plan after you retire.

· Certified Charitable Distributions (QCDs) will nonetheless be permitted beginning at Age 70 ½, permitting you extra time earlier than RMDs start to convey your IRA stability down. Moreover, the present restrict of $100,000/12 months for QCDs will begin adjusting for inflation in 2024 – this represents the potential for important tax financial savings for these retirees who don’t want their RMDs to keep up their existence.

Deal with YOUR Huge Image – Don’t Observe Somebody Else’s Recipe

Whereas the significance of saving is common, your imaginative and prescient and plans for the longer term are uniquely yours and require your individual recipe for fulfillment. These resolving to train extra beginning January 1st will see higher outcomes with a personalized coaching plan they will persist with. Assembly your wealth objectives is not any totally different – information and ideas can by no means change a personalized plan constructed only for you. In case you are into resolutions and haven’t made one but, decide to 2023 being the 12 months that you simply take inventory of your large image and decide if the actions you take are the actions that may efficiently get you to the place you need to be. If they’re, nice! Hold doing what you’re doing and take into consideration what else is likely to be doable. If not, let’s speak about how one can get there…with out the “shoulds” or B.S. pushed by different peoples’ definitions of success.

[ad_2]